“Xoom…. think Western Union without the excessive fees…”

TechCrunch, Sep 28, 2007

Xoom’s two-decade-plus history is full of missed opportunities and second chances. The child of the so-called “PayPal Mafia” and protege of Sequoia Capital, Xoom was founded in 2001 to disrupt cross-border remittances. At that point, Western Union already had a website where customers could initiate and track money transfers, but it was clunky and saw little use. The shift to online remittances was expected imminently, so creating an online-only provider with a better user experience was a no-brainer.

The early years

The Xoom website was formally launched in 2003…

… and its troubles began in its first years, with frequent hiring mistakes and the allocation of significant resources to a B2B pivot that ultimately failed. In 2010, Keith Rabois, an early investor and Board member of Xoom, provided this summary of the early years:

By 2007, six years and five funding rounds later, Xoom had evolved into the business model it is known for today: digital-only instant money transfers and a great user experience. During those early years, Xoom remained a relatively small company, with revenues of less than $20 million, compared to Western Union’s $3 billion. However, the growth strategy was clear and straightforward: persuade customers in as many corridors as possible to try its application.

In the subsequent years, Xoom accelerated its growth, tripling revenues from $26 million in 2009 to $80 million in 2012. Thanks to its strong performance and inclusion on the “Top 50” VC-backed companies list, Xoom was well prepared for an IPO. On the first day of trading in February 2013, Xoom’s stock surged by nearly 60%.

Hitting the wall

The timing for the IPO was impeccable, coinciding with Xoom’s growth slowdown that year. The deceleration was slight in 2013 but became more pronounced in 2014.

With each quarterly result, it became increasingly evident to investors that Xoom wasn’t positioned to become the “next big thing.” The company’s stock started to plummet, falling below its IPO price.

To compound the challenges, Xoom experienced a massive fraud case in late 2014. Xoom disclosed a $30.8 million corporate email/finance department fraud in late 2014; importantly, this was not customer transfer fraud, but it still damaged investor confidence. More crucially, in 2015, the company’s money transfer volumes entered negative territory every other quarter.

Xoom became the slowest-growing digital cross-border money transfer provider among notable players, including the digital divisions of Western Union and MoneyGram:

Xoom today

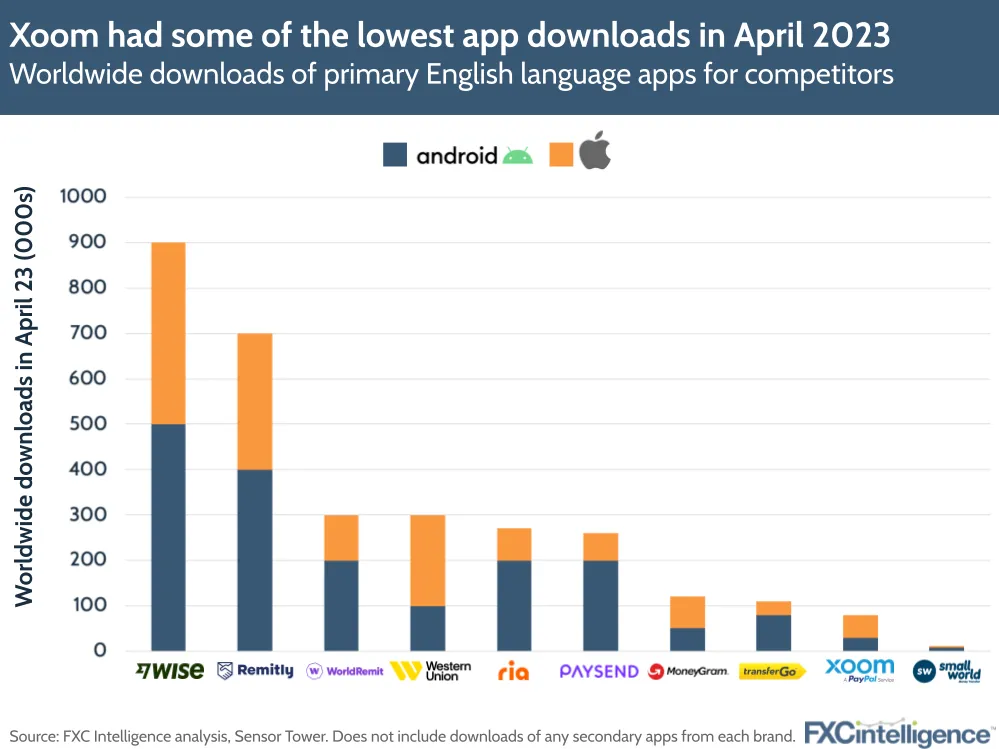

This brings us to Xoom’s current state. The company remains a marginal player in cross-border remittances. Its transaction volumes not only significantly lag those of leading traditional incumbents but also those of newer fintech competitors, such as Remitly, which entered the market a decade after Xoom.

One newer fintech in particular, Wise (formerly known as TransferWise), has achieved remarkable success. It surpassed Xoom’s transfer volumes in 2015, just four years after its inception. By 2022, it had become the world’s largest player in terms of transfer volumes:

Why has Xoom not succeeded in becoming the primary disruptor or achieving a position among the top 10 global players?

Running fast was not fast enough.

Xoom did many things right. Recognizing the importance of robust risk management, the company leveraged customer data to achieve an approval rate of over 90% for transfers linked to customers’ bank accounts—a remarkable achievement at the time. Moreover, Xoom understood the drawbacks of relying solely on online marketing to establish credibility with migrants who were entrusting a new type of provider with their money. To build trust, Xoom invested heavily in traditional TV advertising and tailored its commercials to resonate with diverse ethnic groups, demonstrating a nuanced understanding of its target audience.

Xoom also recognized that pricing was not a critical factor for a large portion of migrants, so it was often one of the more expensive providers in the market.

Moreover, Xoom continually games its FX markups to maximize profits, often at the expense of customer peace of mind. Unfortunately, this practice is common among other providers such as Western Union and MoneyGram, though it’s less prevalent with Remitly and WorldRemit and is not an issue with Wise.

So, why did Xoom hit the wall in 2015? The macro context shifted, and the company failed to adapt. Until 2013, a significant number of tech-savvy, price-sensitive customers were transitioning from expensive wire transfers to remittance providers. These customers, primarily migrants from India or younger European expats, required only a slight push to try out a widely promoted service. However, once this surge of unmet demand was met, digital players like Xoom had to figure out how to alter an individual’s preferred sending method or attract entirely new customers amid growing competition from other digital providers.

Price was starting to matter.

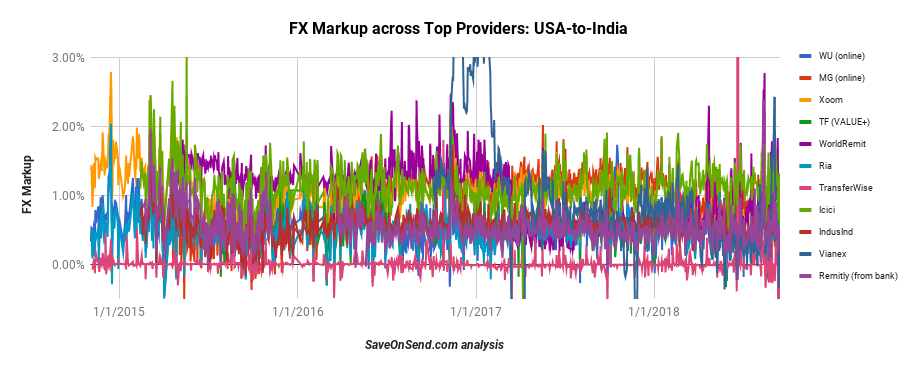

The most widely recognized strategy for gaining market share in a fiercely competitive, uniform environment is to offer lower prices. Although Xoom aimed to maintain its high-profit margins, other providers, including incumbents, reduced their prices in specific corridors, with a noticeable impact (e.g., USA-to-India). Eventually, Xoom reluctantly followed suit – its foreign exchange markups from the US to India dropped to half of those to China, Mexico, and the Philippines. However, this adjustment proved insufficient. The CEO of Xoom elucidated the loss of market share in this corridor during the Q1 2015 earnings call on April 28th (for the complete transcript, find the source here):

“I think what’s going on in India is this, starting in Q3 (2014)… we’ve seen one or two or three names selling rupees between 30 and 70 basis points, and those names include Ria, MoneyGram primarily… it’s hard to see how they can consistently stay down at those rates. But, of course, competition can behave irrationally if they want to.”

However, another quarter passed, and all providers further reduced their margins to even lower levels. Below is a comparison of the change in foreign exchange markups between April 11 and August 11, 2015:

Naturally, faced with the risk of being completely excluded from this critical digital remittances corridor, Xoom had to change its approach. Right after that April 28th statement, the company swiftly dropped its FX markup to all-time lows:

However, since many other providers also followed suit (for instance, TransferWise reduced its fees for this corridor by 40% in October 2015), Xoom’s fees remained significantly higher than those of its top competitors:

This led to an additional loss of market share, as indicated in Xoom’s Q2 2015 report released July 29 29, 2015:

“For example, our competitors have offered coupons for free money transfers and, in India, have offered better exchange rates than we have in certain periods and established no fee services. As a result, we have experienced attrition of rate-sensitive customers, particularly those customers who send money transfers to India.”

When operating on a 1% margin results in a loss of market share, it should underscore the competitive nature of digital remittances. But how were Xoom’s competitors able to “behave irrationally”? At that time, traditional players still conducted 90% of their business through higher-margin cash agents. Meanwhile, certain fintechs like TransferWise and Remitly had more streamlined operating models, enabling them to pass on savings to their customers.

In late July 2015, Xoom adopted a peculiar advertising strategy of frequently promoting “best ever” rates to stem the tide of market loss. These rates were deemed “best” not due to a reduction in Xoom’s FX markup, but simply because of a higher dollar-rupee exchange rate prevailing in the market at that time:

Xoom’s market share decline within the crucial USA-India corridor persisted. In response, the company reduced FX margins for transfers exceeding $2,000 in August 2017. The irony of this threshold was apparent, given PayPal’s CEO, Dan Schulman, nauseating preaching for financial democratization to combat poverty. While virtue signaling is often the end objective of Western executives, rather than fostering genuine change, it also redirects media attention away from the company’s actual profit-generating methods:

America First backfires

Another factor contributing to the Xoom slowdown was the limited number of corridors it had launched by early 2015. Serving 37 countries outbound from the US seemed respectable at the time, particularly given that US residents account for around 20% of the world’s remittances. However, this coverage was incomparable to the extensive digital remittance network offered by incumbents like Western Union (SaveOnSend article for more details):

Remittance startups like TransferWise and WorldRemit also surpassed Xoom in the number of corridors they serve. Initially, Xoom’s operating solely out of the US might have been a logical strategy, given the substantial growth potential in the world’s largest outbound market. However, this approach did not align with investors’ scaling expectations for a high-flying fintech IPO. Xoom’s management appeared fatigued and unwilling to accelerate growth, experiment, and learn new operating muscles.

White knight on a white horse

The news of PayPal’s acquisition of Xoom wasn’t entirely unexpected. Xoom’s leadership and board members were aware of their circumstances and had attempted to sell the company since mid-2014, reaching out to various potential buyers without success. Given the shared origins of Xoom and PayPal, as well as their investors and board members, the merger was anticipated.

However, the acquisition details were astonishing: PayPal paid an 80% premium for a company experiencing a rapid performance decline. By early April 2015, Xoom’s stock had stabilized at around $14, but acquisition rumors were beginning to drive its price higher. This trend continued even after the disclosure of Q1 2015 results, revealing a mere 6% year-over-year growth in transfer volume, significantly lower than the previous year’s 49%. Typically, stocks that surge due to acquisition rumors are purchased at their value on the day of the acquisition. However, PayPal unexpectedly paid an additional 20%+ premium on top of the already massively elevated stock price.

Moreover, although there was no single alternative bidder, PayPal didn’t try to negotiate Xoom’s asking price. Finally, because PayPal was roughly 40 times larger than Xoom, it had no urgency to pursue this acquisition. Instead of moving forward, they could have waited for another couple of quarters to see if Xoom could reverse the slowdown in growth. Just imagine where Xoom’s stock price might have been after the company announced a decline in transfer volumes in late July 2015.

What could have been the rational reason for the above? According to PayPal’s CEO:

“Acquiring Xoom allows PayPal to offer a broader range of services to our global customer base, increase customer engagement and enter an important and growing adjacent marketplace. Xoom’s presence in 37 countries – in particular, Mexico, India, the Philippines, China and Brazil – will help us accelerate our expansion in these important markets.”

Each point in that statement was misleading:

- PayPal was already offering cross-border money transfers to consumers and didn’t need Xoom to start offering this service. By maintaining a relatively high FX markup, PayPal had chosen not to compete aggressively in this space. This was precisely why Xoom planned to continue operating as a “separate service” after PayPal’s acquisition. Why wouldn’t PayPal offer the convenience of a single platform for all possible customer needs? Similar to its approach to separating Venmo, PayPal wanted to preserve high margins for its core business-related transfers.

- It’s the same story with “increase customer engagement.” Xoom was losing market share, and even among its existing customers, the average transfer amount had dropped 17% compared to a year before the acquisition. How exactly could PayPal’s customer engagement benefit from this track record?

- Finally, Xoom did not have a real presence in other countries in 2015. Fundamentally different from providers with local field offices, Xoom had contracts with local banks or retail chains to distribute funds and, in some countries, Xoom even worked via 3rd parties like Earthport to obtain such service. How would those contracts with Xoom “accelerate” PayPal’s expansion in those markets, and in that case, why wouldn’t it just sign its agreements with intermediaries like Earthport? Wouldn’t that ensure much faster expansion and be cheaper than spending almost one billion dollars on Xoom?

The more plausible explanation is timing. PayPal was separating from eBay and needed a clean, independent company growth narrative: mobile, Venmo, merchant payments, and now global remittances. Xoom gave PayPal an instant remittance story — 1.3 million active US customers, roughly $7B of annual volume, and 37 receiving countries — even though the operating data already showed slowing growth.

Xoom’s performance since PayPal’s acquisition

In 2016, Xoom’s revenue reached approximately $185 million, representing a less-than-10 % increase over the previous year. By November 2017, Xoom attempted to put a positive spin on its performance, citing vanity metrics while withholding details about its revenues or transfer volumes. Behind this lackluster growth was an increasingly odd focus on outbound corridors from the United States.

During that period, Xoom expanded its coverage to 67 destinations, adding one destination in Q1 2017 and 11 more in Q2 and Q3. However, all were limited to outbound transfers from the US. Can you guess the impact of adding the 67th country, outside the US, even assuming a massive 20% market share? Less than 0.5% in additional transfer volume.

Only in December 2018, over a decade after formally focusing on remittances, did Xoom launch its second outbound country, Canada. It wasn’t until July 2019 that Xoom announced the addition of 32 European countries. In contrast, newer fintechs added outbound countries in less than half the time.

The integration with PayPal wasn’t progressing rapidly either. It took 11 months after completing Xoom’s acquisition, with PayPal finally announcing integrated workflows in October 2016, supposedly offering Xoom as one of the transfer options to its customers:

In reality, PayPal customers would observe more transfer options on the initial screen. However, for the actual transaction, they would still need to use a separate Xoom application:

With Xoom’s stagnant business performance, PayPal ceased to share any valuable data, dropping instead to the relative performance of vanity metrics such as Net New Actives (NNA):

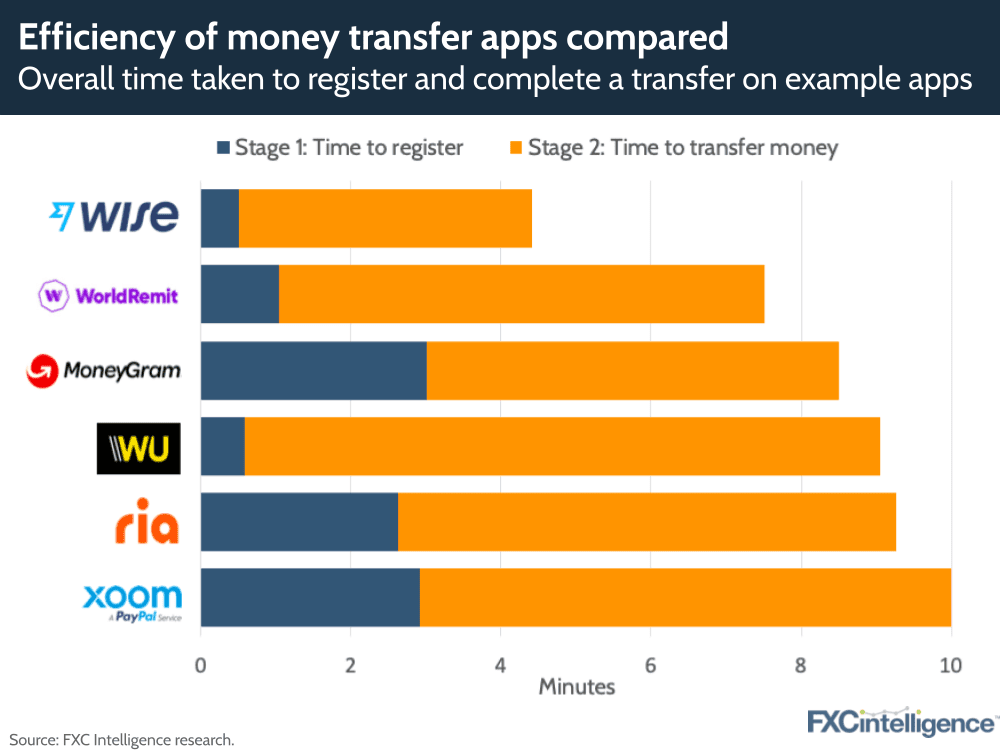

As years went by, Xoom’s financial results remained stagnant, while the price and quality of its offering remained among the worst among digital competitors:

By late 2023, PayPal’s stock had fallen roughly 80% from its peak; Alex Chriss had replaced Dan Schulman. Rumors surfaced that Xoom could be sold. By 2026, even that turnaround had failed to satisfy investors, with Enrique Lores replacing Chriss, making Xoom look even less like a strategic asset PayPal could monetize at anything close to its original purchase price. While Wise and Remitly were valued at around $12 and $4 billion, respectively, it was unclear if PayPal could recoup its original $1 billion investment.

Xoom jumps on the crypto bandwagon.

In August 2023, PayPal announced the launch of its stablecoin, PYUSD. Of course, every company wants to print its own money at no cost to capital as long as there are willing buyers. PayPal’s marketing strategy was to publicize PYUSD as enabling fee-free cross-border transfers through Xoom, a service it launched in early 2024.

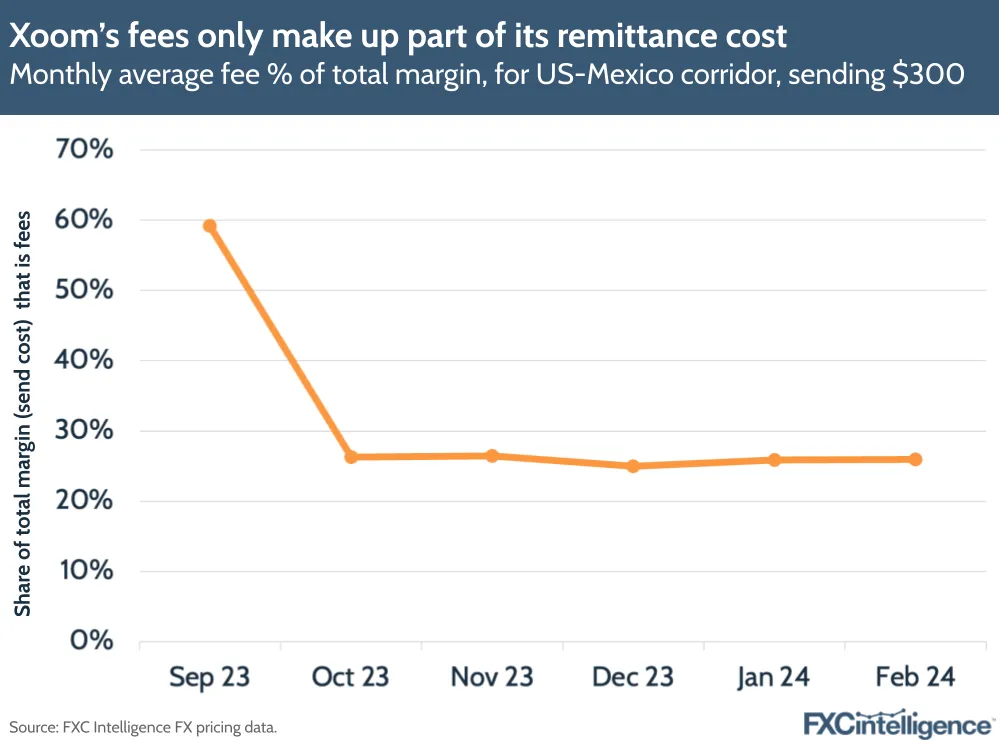

Of course, the service was never truly free. PayPal could remove the visible fee while preserving, or even increasing, the less visible FX spread. PYUSD also gave PayPal a remittance use case for its stablecoin and a reason for customers to hold balances inside PayPal’s ecosystem rather than cashing out immediately. Xoom made twice as much money on the FX markup, and it could simply increase this further while eliminating more visible fees:

Why were Xoom customers asked to select a stablecoin rail as a payment method? If transferring money via PYUSD is much faster and cheaper than SWIFT and ACH, why wouldn’t PayPal replace those fiat methods with a stablecoin one for all transactions? It’s not like consumers know or care which back-office protocols a company uses to provision their financial or insurance services.

The answer is straightforward: PayPal does not want to cannibalize its profit margins, since Xoom is usually among the more expensive MTOs. Instead, it hopes to attract additional customers and keep them holding PYUSD rather than cashing out immediately, thereby providing PayPal with free capital. Furthermore, such PR efforts create the perception of a genuine use case for their stablecoin, making it a worthwhile investment even for consumers and businesses without any remittance needs.

In Conclusion

Thank you for reading. As with all of our analyses, this article will be updated regularly, so please check back with us frequently or after major news. If you think we got anything wrong or if you know why PayPal acquired Xoom in such an unusual way, please share your thoughts in the comments section below.