“High fees, large incumbents, and a $400B+ market are under attack by a slew of remittance startups.”

CB Insights, February 26, 2015

For disruption to occur, it only takes one determined startup with a long-term vision spanning two or more decades. The disruptive force of innovation only requires one Amazon for books, one Spotify for music, and one Netflix for entertainment. After over two decades since Xoom’s founding, the first fintech in this space, two fintechs ended up ahead of the pack. More than a decade of keen observations in this fiercely competitive space has given us a reasonable understanding of what made Wise and Remitly so far ahead of others, and why some fintechs are no longer around.

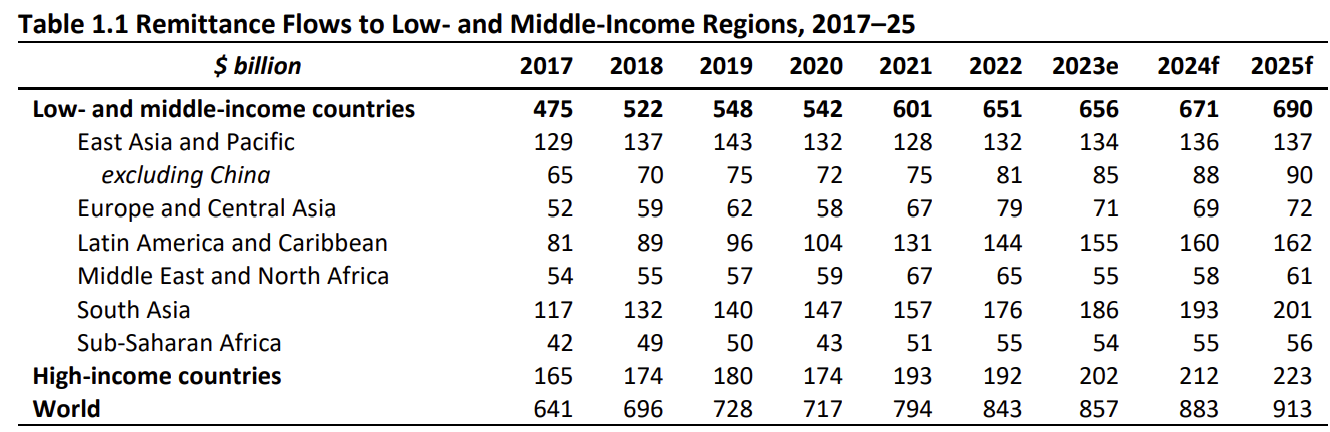

The good news for fintechs over the last decade has been that the market has continued to grow. FXCintelligence estimated the overall C2C cross-border market at $1.8 trillion in 2024 and forecasted it to grow 9% in the foreseeable future. In remittances alone, the volume has been increasing by $25-50 billion annually, and the World Bank conservatively projects a 3% annual growth rate in the coming years.

The bad news is that the transition in consumer habits towards embracing fintechs and digital channels has been gradual. A decade ago, conventional wisdom suggested that the widespread availability of affordable smartphones and the shift from tech-averse elders to tech-savvy millennials would lead to a rapid increase in the use of online channels for cross-border money transfers.

Three years later, in 2018, some of the same folks were predicting that cash agents would completely vanish within the next five years:

Not only did none of that transpire, but in 2022 Azimo’s struggles led to its acquisition by a payroll company to salvage parts of its payment technology. The competition among money transfer players has proven significantly more challenging than initially expected, while incumbent banks and MTOs have proven significantly more resilient.

Money Transfer “Disruptors”

Around 2010, the potential to disrupt consumer cross-border money transfers seemed enormous. The prevailing perception was that established players like Western Union, MoneyGram, and Ria were committed to their brick-and-mortar branches and might be unwilling or unable to provide consumers with a more streamlined digital alternative. Xoom had been in the market for a few years and was experiencing significant growth, but it only targeted outbound corridors from the United States. Moreover, given the market’s immense size, it seemed feasible to accommodate multiple fintechs, especially during the early stages of the digital revolution.

Hence, the aspiration to become a larger, superior alternative to Western Union didn’t seem too daunting. So, a new generation of fintech founders challenged the CEOs of established money transfer businesses.

Bottom row: Ria Money Transfer, MoneyGram, Western Union Digital Ventures, Xoom, Transfast

Some of the noteworthy startups that emerged during those years were:

- Zepz, aka WorldRemit (founded in 2009)

- TransferWise (2011)

- Remitly (2011)

- Azimo (2012)

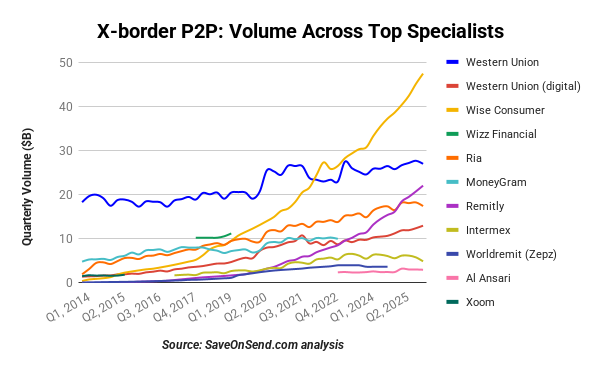

While Azimo is no longer around, Wise passed Western Union’s transfer volumes in 2022, and Remitly has inched closer to overtaking Western Union volumes:

Has the disruption affected traditional players so far?

Western Union has more than doubled its transfer volumes since the early days of Xoom (the original fintech for remittances). However, this growth wasn’t sufficient to keep pace with the expanding market, leading to a gradual erosion in its market share of remittances over almost two decades:

Another sign of the collective impact as fintechs achieved scale is the decline in incumbents’ margins, commonly known as the “take rate.” Before fintechs reached scale in 2020, incumbents paid little attention to this aspect. Here’s how the CEOs of Western Union and Euronet (the parent company of Ria Money Transfer) described the competitive pricing environment in 2018:

In 2020, Western Union’s margin declined by over 20%, falling from around 5% to less than 4%. This was driven in part by price reductions and the gradual expansion of the share of less expensive digital transfers. Other incumbents also reduced their margins, while those of Wise and Remitly remained relatively stable:

The second-largest incumbent, Ria Money Transfer, has also not experienced disruption yet, but its revenue growth rates, which were previously around 20%, have now decreased to low single digits:

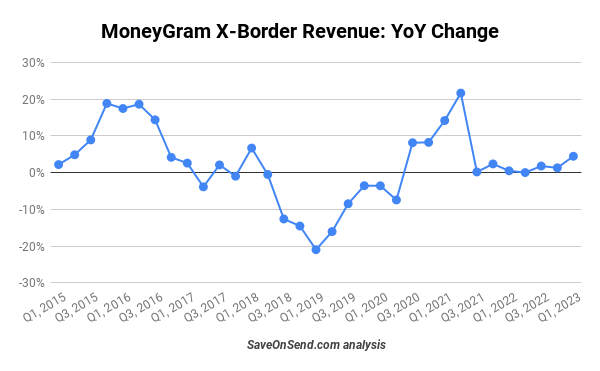

MoneyGram, once the second-largest incumbent in the industry after Western Union, is in a stable state now but is grappling with a lack of growth after a near-death experience in 2019 (as discussed in this SaveOnSend article):

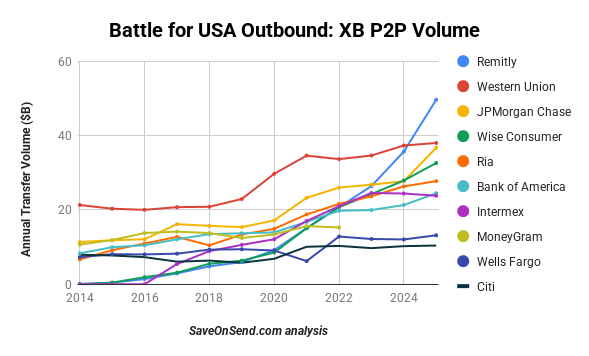

In addition to traditional money transfer operators, banks play a significant role in cross-border money transfers. Consumers in the US send more than $100 billion annually via banks. Banks have yet to experience disruption and have nearly doubled their transfer volumes in the last decade (for more information, refer to this SaveOnSend article). The largest consumer bank in the US, JPMorgan Chase, has remained among the top 3 players:

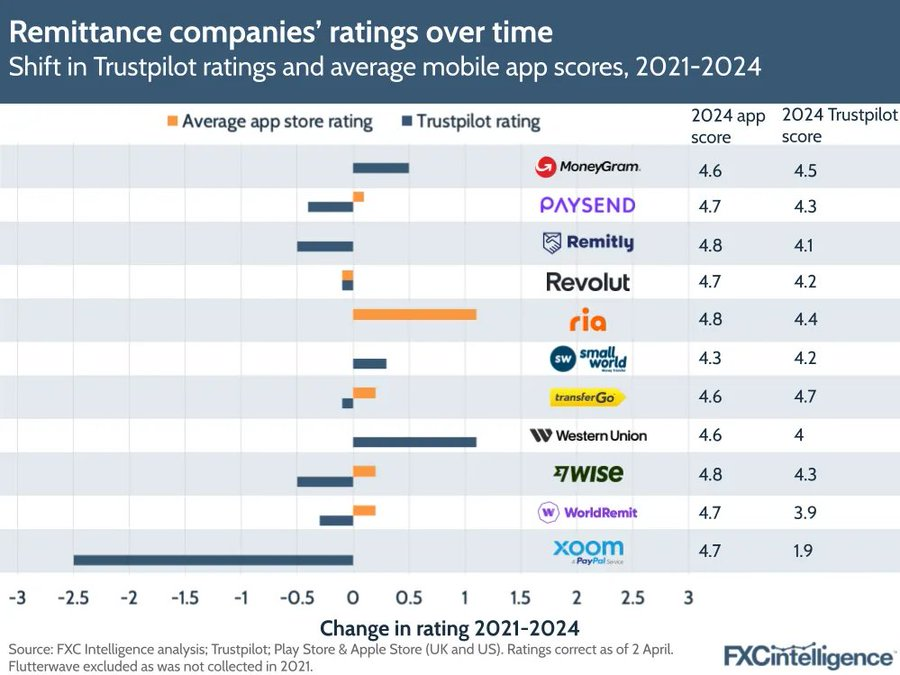

The lack of disruption so far is partly caused by traditional players not standing still. They are typically slower than fintechs in launching new features, but eventually, they catch up by observing startups and copying what works. For example, between 2021 and 2024, the Trustpilot rating of traditional players has improved, while that of fintechs has declined, making the two groups indistinguishable regarding customer satisfaction:

The crucial role of focus in disruption

As Jim Barksdale, CEO of Netscape (the world’s largest browser at the time), famously said in 1995, “… there are only two ways I know of to make money: bundling and unbundling.” Fintechs are generating revenue by unbundling incumbents until they reach a sufficient size to begin bundling additional products. Subsequently, new fintechs emerge to unbundle the previous generation. In cross-border consumer money transfers, Xoom and Remitly were introduced to unbundle Western Union; Wise to unbundle banks; and new fintechs keep launching to unbundle Wise and Remitly.

One of the most challenging dilemmas for a growing fintech company revolves around the timing of bundling new products and entering new regions. With the rise in product and geographical complexity, founders and key employees may find their attention stretched too thin. Additionally, they might become disengaged from the core product, especially if its growth begins to slow, and prefer to work on a new internal venture with higher growth potential. A straightforward way to determine whether bundling is premature is to examine the core product’s growth rate to see whether it’s decelerating rapidly or gradually.

In recent quarters, Remitly and Wise have stabilized cross-border money transfer volume growth at around 40% and 20%, respectively. Since the market is growing less than 10%, with their massive scale, their sustained focus could maintain those growth rates and push incumbents among banks and MTOs out of business.

Money transfer funding and valuation

The appeal of disruption and the substantial assets held by VC firms ensured an abundance of capital available to fintechs in this space. Between 2010 and 2019, just four startups attracted over $1.5 billion in funding:

As is customary with faster-growing fintechs, they command higher valuation multiples. For instance, the valuations per unit of transfer volume for Wise and Remitly are two to four times higher than those of Western Union and Intermex:

While there hasn’t been a disruption in incumbents’ volumes yet, it is fascinating to note that the value of Wise and Remitly, which didn’t exist before 2011, is now much higher than that of Western Union. Investors are clear about which types of companies have much higher potential in cross-border consumer money transfers.

Performance differences across fintechs

After a couple of years, investors began distinguishing fintechs by the quality of their performance, encompassing their business, operational, and technological models. When examining the speed and scale of funding rounds from their launch, Wise had significantly outpaced the competition by Year 3. Remitly and WorldRemit were striving to keep pace with varying degrees of success, while Azimo never entirely gained traction:

By September 2018, Remitly had reached $6 billion in annualized transfers. While this might appear substantial, it paled compared to TransferWise’s growth trajectory. Both companies were founded around the same time and received their first $1 million+ in funding in April 2012. However, TransferWise reached a $2 million monthly transfer volume just a year later, more than two years ahead of Remitly. By mid-2015, TransferWise was transferring thirty times more per month than Remitly:

The underlying reason is in Remitly’s much slower scaling. In the first three years after Remitly was launched, the fintech served only one corridor: USA-to-Philippines. In February 2015, Remitly launched the second corridor, USA-to-India, and in October 2015, the USA-to-Mexico corridor. In July 2015, Remitly also announced its first acquisition of a failing application, Talio, to bring in local talent (both companies are based in Seattle) and beef up messaging features in Remitly’s mobile technology. In April 2016, Remitly opened an outbound business from Canada to India and the Philippines. In September 2016, the startup added seven more countries in Latin America for transfers from the US:

In early 2017, Remitly expanded its services to include a couple of outbound corridors from the UK. Given the excitement surrounding the digital remittances niche, it was not surprising that in the October 2017 funding round, Remitly was valued at “at least” $345 million.

Remitly utilized the funding to expand into new markets, such as Australia, in May 2018. By July 2019, Remitly had operations in 16 countries and had surpassed $2 billion in quarterly transfer volume:

While Remitly’s progress is commendable, it is overshadowed by TransferWise’s rapid expansion. TransferWise launched hundreds of corridors in the first four years, reaching $1 billion in transfers within its first 12 months in the US alone. By mid-2019, TransferWise handled seven times more volume than Remitly, with only 60% more employees. By 2021, TransferWise had expanded to cover over 40 outbound countries.

… while Remitly covered only 17:

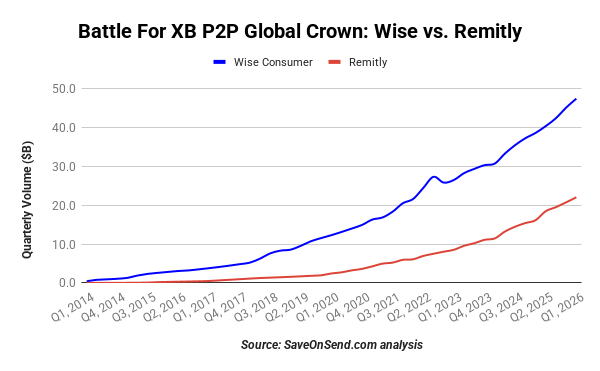

Since Wise handles more than twice Remitly’s consumer cross-border transfer volume while growing 20+% vs. Remitly’s <40%, the gap between the two leading fintechs continues to widen. Every quarter, Wise was $10 billion ahead of Remitly in XB P2P volume in 2020, $20 billion in 2024, and $25 billion in 2026:

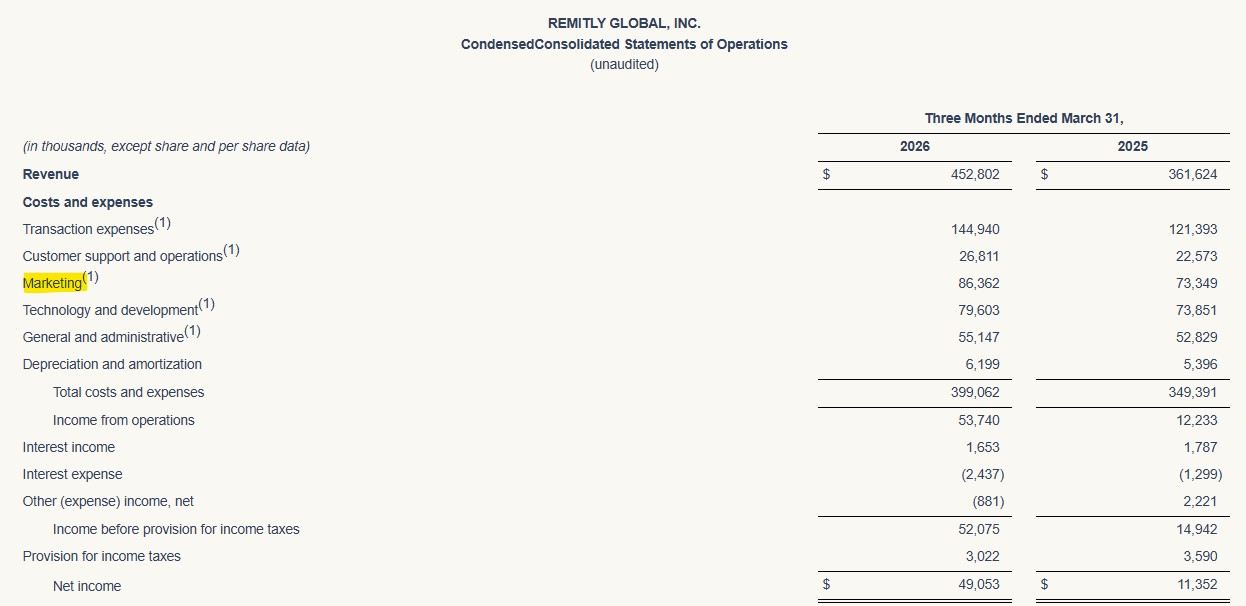

Wise prides itself on a low-cost referral channel (aka paid “word of mouth”) that accounts for 70% of its growth, while spending only 4% of revenue on marketing. Wise could theoretically increase its marketing spend if its volume growth rate starts slipping below 20%. Remitly, on the other hand, has historically maintained its 35-40% volume growth rate by spending around 2o% of its revenues on marketing. As a result, it is on track to finally turn a profit only in 2025.

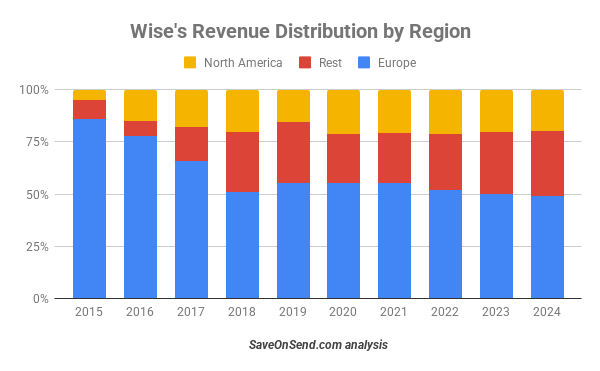

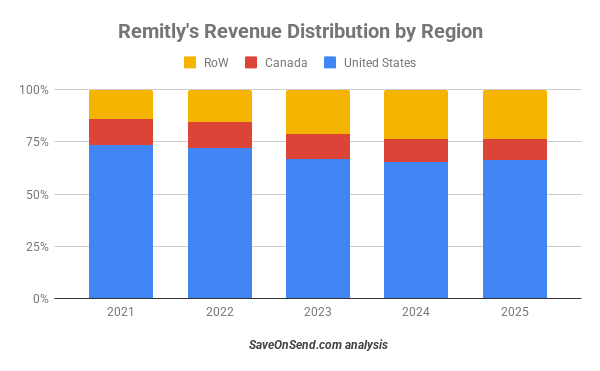

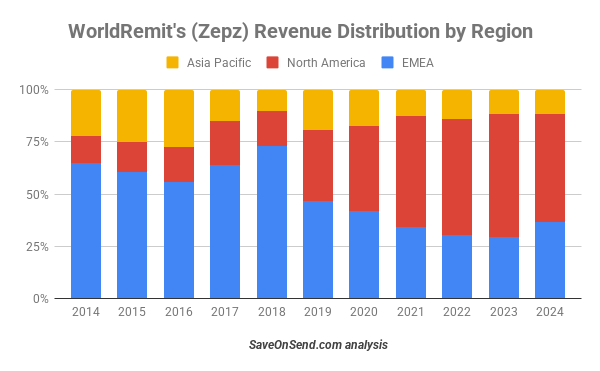

Wise’s larger transfer volumes and faster global expansion have resulted in more diversified regional revenue than Remitly. However, what’s notable in recent years is how stable these regional splits remain at scale, even as both fintechs continue to grow by 20-40%.

Why do money transfer fintechs fail?

A successful fintech typically takes five years to achieve profitability, requiring hundreds of millions of dollars in interim investments to acquire millions of customers. VC firms step in to fund this cash flow gap. Given that most fintechs fail, VCs are only willing to take such significant investment risks if they believe the fintech has the potential to become a market leader, at least in one large region. Remitly was primarily seen as a player in the US outbound market, WorldRemit in the Africa inbound market, and Wise in the Europe outbound market.

Unfortunately for Azimo, it began operations a year after Wise with a similar regional focus. While its customer base comprised blue-collar migrants, Wise’s remarkable growth, compared to its focus on white-collar expats, indicated to investors that all types of cross-border consumers would eventually be interested in its service.

However, Azimo’s slower growth compared to Wise wasn’t solely due to the one-year lag. It was also attributed to less capable leadership, although the comparison was against an extremely high bar. Unlike Wise and Remitly, which achieved comparable success, the Azimo founders appeared more inclined to speak at conferences about their achievements and to make unsupported statements about the imminent disappearance of offline channels. Instead of actively acquiring new customers, they seemed to rely on the digital wave to bring them customers.

Even more unusually, the lack of intensity manifested in Azimo openly discussing its desire to be acquired as early as 2015, just three years after launch. The negative impact of Azimo’s less competent management team and lower intensity relative to leading fintech competitors was exacerbated by the sudden 2017 exit of a co-founder, whom employees described as the “heart and soul of the place.”

Similar to Xoom, Azimo also limited its growth ambitions to just one outbound geography (in Azimo’s case, Europe, whereas for Xoom, North America for the first decade). As a result, Azimo’s growth slowed down to 25% by 2020, even as expenses increased by 50%:

While investors were willing to provide hundreds of millions of dollars to Wise, Remitly, and WorldRemit, Azimo’s final funding round in May 2018 amounted to only $20 million, and the underlying valuation wasn’t disclosed. In early 2022, Azimo was acquired by a payroll payments company at a valuation similar to its 2018 valuation.

TransferGo and WorldRemit (Zepz)

A somewhat similar fate met another Europe-based startup, TransferGo, although it is still in operation. The startup was founded a year after Wise by Lithuanians who openly admitted they were trying to clone their Estonian competitor. While Wise was small enough and the market was expanding, TransferGo managed to grow rapidly, with a 100% growth rate in 2018:

By 2021, TransferGo’s growth slowed to 25%, with a cumulative volume of $6 billion over the previous almost decade. Remitly was already transferring $6 billion annually, not in total, three years earlier. Wise crossed $6 billion in cumulative transfer volume in 2015, six years before TransferGo. In 2022, its primary UK subsidiary showed declining revenues and increasing losses. In 2024, 12 years into existence, TransferGo raised only $10 million without disclosing its performance.

WorldRemit (aka Zepz) falls into a middle-ground category, being more successful than Azimo but trailing behind Wise and Remitly. The underlying reason for its lower valuation compared to the leading fintechs is essentially the same: relatively weak planning and execution. For instance, in 2015, WorldRemit significantly overestimated the speed of its growth across markets, leading to employee layoffs in the US and the UK.

In 2017, WorldRemit was eager to expand in the US and drastically cut prices by two-thirds in its two top corridors, resulting in a loss of approximately 0.5% per transaction. However, realizing that this strategy wasn’t working or sustainable, WorldRemit eventually raised its prices back to previous levels:

Mistakes in regional expansion efforts cost years of hard work and resulted in a combined market share outside of Europe that was lower in 2018 than it was in 2014, only starting to recover afterward. In 2020, WorldRemit agreed to buy Sendwave near the peak of the Covid digital remittance boom to acquire a fast-growing, app-only franchise in North America-to-Africa corridors. This growth did not translate into durable profitability: losses remained large after the deal, and by 2024 Zepz was explicitly prioritizing sustainable growth, cost reduction, consolidation of WorldRemit and Sendwave, and lower headcount. Ironically, Sendwave was pruned most aggressively, so the North America share began to decline again.

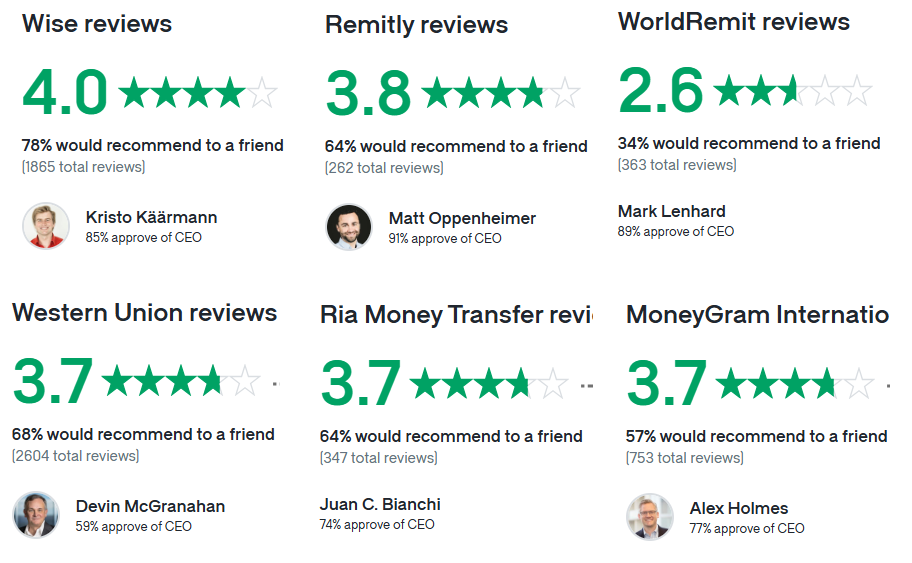

The performance gap is also evidenced by a critical difference in employee reviews of working for WorldRemit versus other fintechs and traditional MTOs:

WorldRemit’s uneven management also led to forecasting misses. In June 2015, its founder & CEO expected to triple 2015 revenue compared to 2014. In November, WorldRemit downgraded expectations to “at least double” and finished 2015 with an 80% growth.

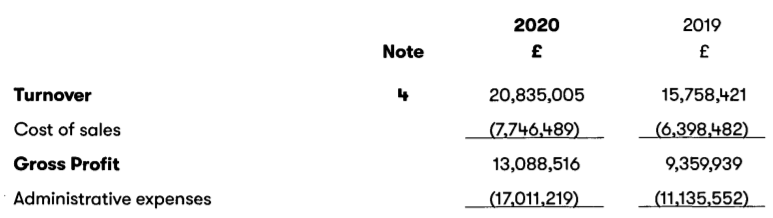

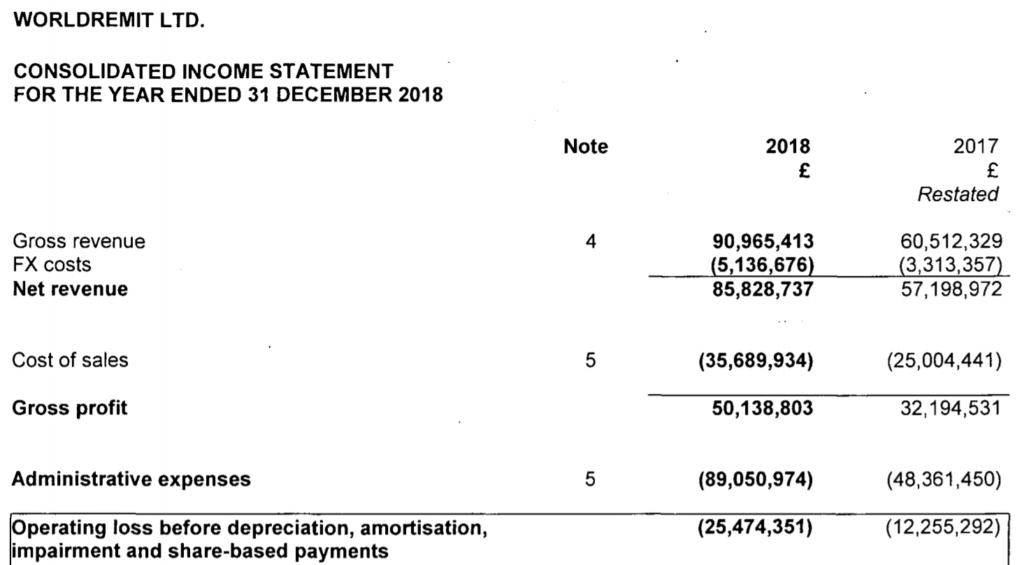

WorldRemit also underperformed in developing a scalable business model. A company growing by 50% should be enjoying rapidly increasing operating margins. However, WorldRemit doubled its losses between 2017 and 2018:

What was even more uncharacteristic for a near-unicorn fintech is that to address its management deficiencies, WorldRemit was spending millions on management consultants, tripling the spending to $8.5 million in 2018:

More fundamentally, in its growth strategy, WorldRemit faced a dilemma similar to Remitly’s until 2021: it was growing rapidly but remained unprofitable, spending almost 25% of revenue on marketing. In 2022, under pressure from investors, WorldRemit had to cut its marketing spending to 13% of revenue. Not surprisingly, that resulted in a collapsing growth rate of just 14%. Its 2023 performance was even worse, with 5% revenue growth on only 11% volume growth and rapidly expanding operating and income losses. By 2024, WorldRemit had effectively stopped pretending this was still a high-growth story: revenue declined by 12%, volume fell by 8%, and the company aggressively cut costs, reducing losses from $88.5 million to $40.0 million.

New players joining the consumer cross-border money transfer game

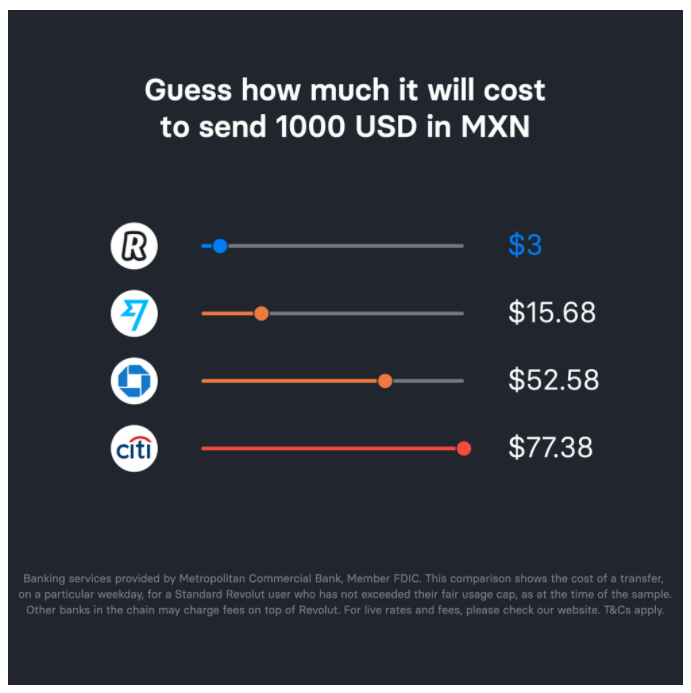

One might assume that the competitive nature of the money transfers for consumers would dissuade other fintechs from entering the market. However, that hasn’t been the case. In 2021, Revolut ventured into the world’s largest remittances corridor, from the US to Mexico (worth over $60 billion), by offering nearly free transfers with no foreign exchange markup to its customers:

The impact was so strong that MoneyGram had to acknowledge it publicly:

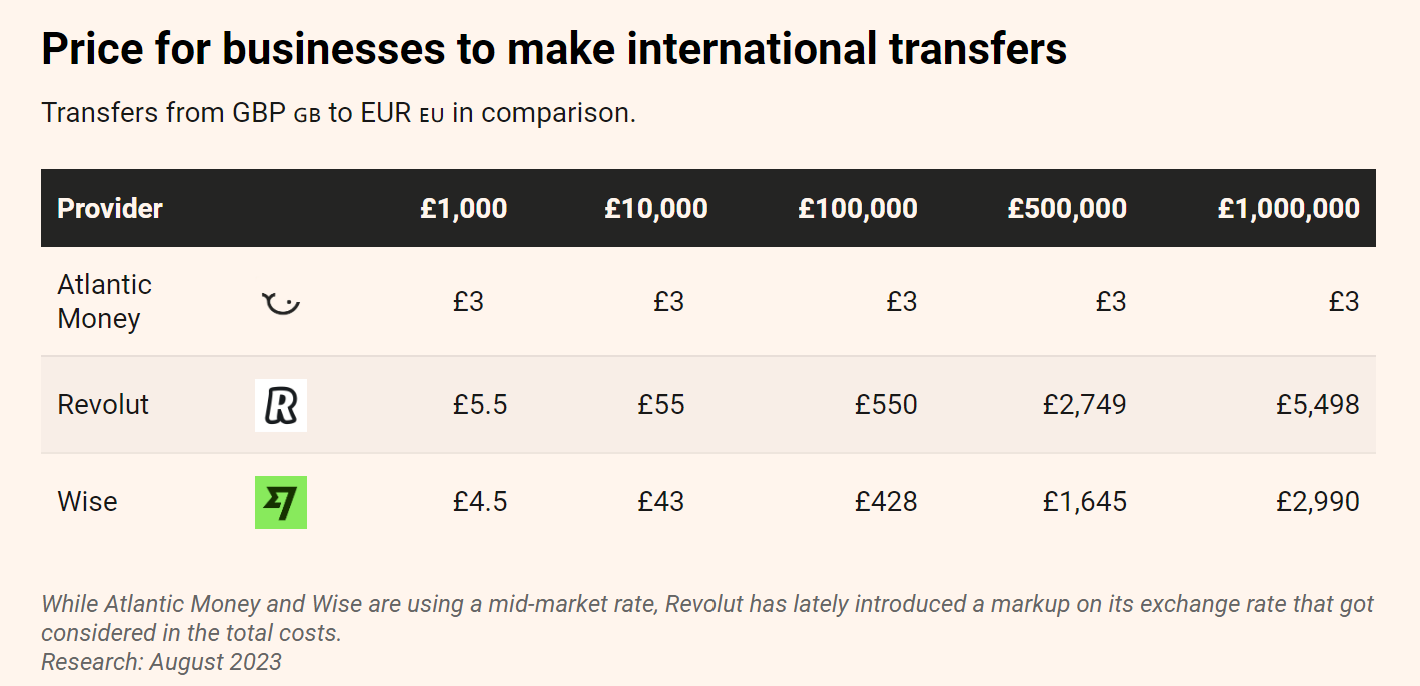

In 2020, Atlantic Money was introduced in the UK by former employees of renowned fintechs, Robinhood and Tinkoff. Their marketing approach aimed to compete directly with Wise. Atlantic Money offered fixed-fee transfers for £3 or €3 at the prevailing exchange rate (eliminating foreign exchange markup):

After 1.5 years, Atlantic Money was running one year ahead of Wise, which passed the same £30M/month milestone around the 2.5-year mark. Additionally, Atlantic Money planned to expand to the US three years sooner. Its tiny fee and zero FX markup were naturally attracting higher send amounts:

Atlantic Money questioned the premise of variable costs for cross-border money transfers. Do the costs actually increase with larger amounts? And if they are more or less fixed, why should providers charge more depending on the amount?

An even more surprising entry into the market came from HSBC’s subsidiary Zing. Launched in early 2024, Zing charges only 0.2% across all corridors with no additional fees and offers more lucrative promotions, including better referral bonuses than Wise. Despite the failure of similar efforts by BBVA (Tuyyo) and Santander (PagoFx), HSBC has wholeheartedly jumped into this highly competitive field, and no less than on the home turf of intense players like Wise, Revolut, and Atlantic Money. True to its scale, HSBC launched Zing with a massive group of 80 employees, supporting transfers in dozens of currencies.

While great for consumers, such intense price competition has raised concerns about the sustainability of new entrants’ business models. It took Wise six years to reach profitability, and Remitly aims to achieve that after 14 years. However, Atlantic Money and HSBC’s Zing were charging much less than these leading fintechs, putting additional pressure on margins and long-term viability. Indeed, by late 2024, Atlantic Money had been acquired by a payroll platform, and by early 2025, HSBC had shut down Zing.

More recently, stablecoin-based remittance players like Felix and Aspora entered the scene, claiming even faster scaling. Considering the deliberately opaque nature of stablecoin transfers, it is too early to know whether those claims are accurate evidence of a superior business model or mostly regulatory arbitrage.

The disruption in international money transfers never seems to stop, so let’s stay alert for more surprises: Banks ← Western Union ← Xoom ← Wise / Remitly ← Who is Next?

Conclusion

Hopefully, this overview helped you understand which players will become the dominant leaders in consumer cross-border money transfers. As with all our analyses, if you encounter any errors or believe we’ve missed essential perspectives in this article, please don’t hesitate to comment below. We value your feedback and will continually update this post, so check back soon for more insights!