“Revolution is a rough business. You can’t make it wearing white gloves and with clean hands”

Lenin

Wise’s (ex-TransferWise) origins are often described as follows: Two Estonians, a former Skype employee, and a Deloitte consultant became fed up with the exorbitant fees charged by banks for money transfers from the UK to Estonia. Fueled by their frustration, they had a stroke of brilliance – matching remittance senders and receivers within the same country. With a sauna in their office and a team unafraid to challenge the banking industry, TransferWise was born. The startup received backing from prominent investors such as Peter Thiel, Richard Branson, and Ben Horowitz, propelling it to the pinnacle of fintech for cross-border consumer transfers, surpassing a $10 billion valuation in 2021, and transferring by far more volume than any incumbent or fintech.

The foundation of PR pitches for money transfer startups centers on a relatively intuitive concept about the role of banks: they are massive institutions with bureaucratic cultures, subpar customer service, and outdated digital capabilities. Consequently, it’s only a matter of time before banks are displaced from the cross-border money transfer industry. Ironically, this premise holds. A typical bank is usually behind in service quality and pricing compared to the leading fintech startups. Furthermore, most banks don’t consider a money transfer business strategic.

Digital-dollar access: buying or holding stablecoins without transferring them internationally.

Consumer remittance: an individual sends money to another individual.

Business payment or treasury: companies move working capital, supplier payments, or FX liquidity.

Wholesale settlement: regulated institutions settle obligations between themselves.

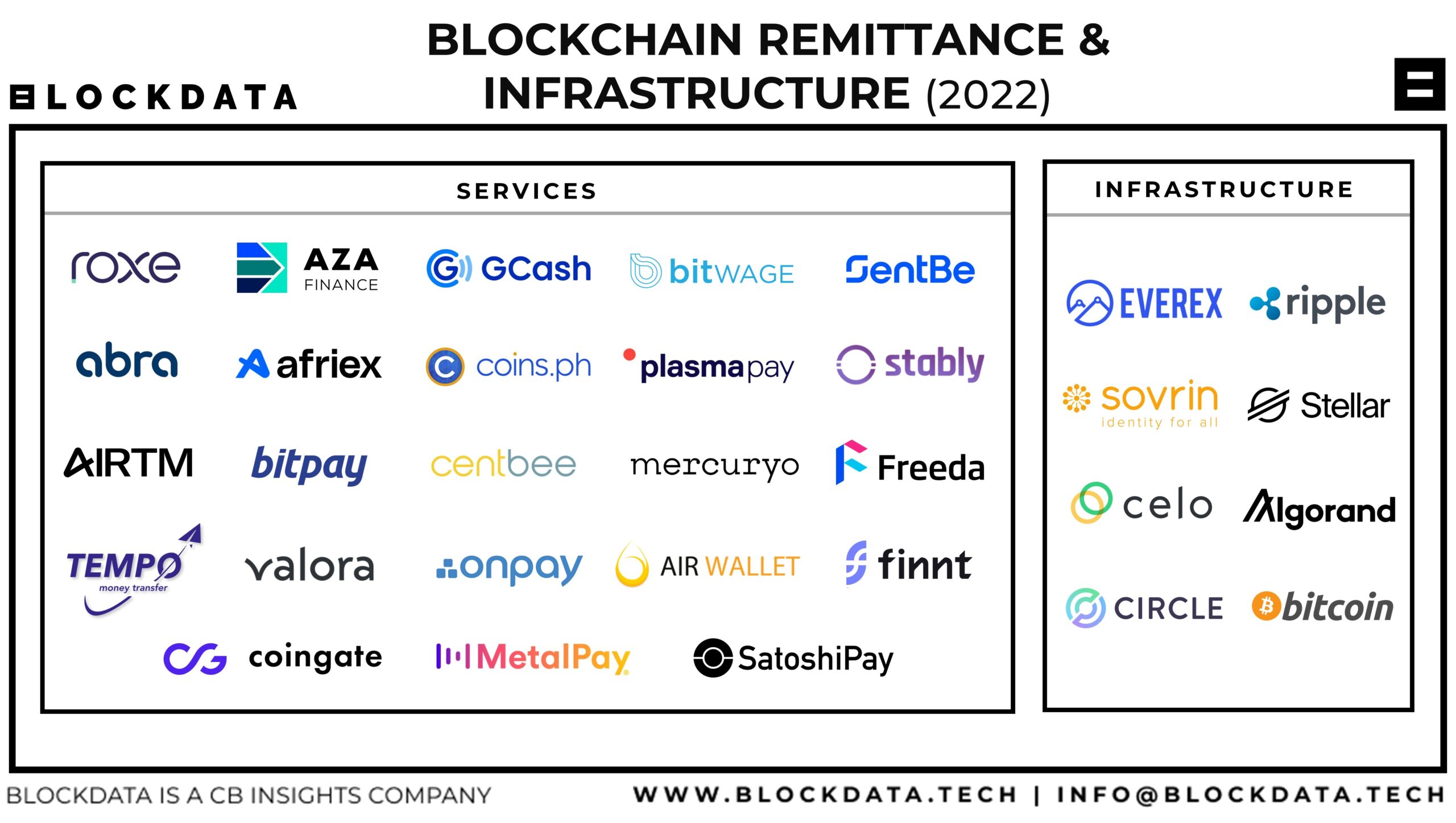

Blockchain infrastructure: the ledger or messaging layer, regardless of the currency transferred.

Since the publication of “Bitcoin: A Peer-to-Peer Electronic Cash System” in 2008, international money transfers, although constituting a smaller portion of cross-border payments, have emerged as one of the most promising use cases for crypto.

The original thesis was simple: remittance users paid high prices for slow, opaque service, while blockchain could move value almost instantly at negligible rail cost. Crypto founders and investors also framed it as a way to bypass banks and reach underserved recipients. Startups raised capital to test that thesis through consumer services and MTO partnerships. El Salvador later turned it into a national experiment by making Bitcoin legal tender and promoting it for remittances.

After more than a decade of pilots, crypto has not displaced conventional consumer-remittance rails at meaningful, independently verified scale. Stablecoins have nevertheless become a credible back-end option in selected corridors and a useful instrument for digital-dollar access, treasury mobility and some high-friction cross-border flows. Most disclosed consumer-remittance implementations remain selective routes, subsidized programs or company-reported deployments whose scale and unit economics are not independently verifiable.

The decisive question is therefore where the full end-to-end system, including funding, FX, compliance, liquidity, payout, cash-out, support, fraud and reversibility, beats modern fiat alternatives on price, speed, reliability and scale. Public evidence remains strongest for digital-dollar access and some business or treasury use cases, and weakest for broad consumer-remittance transformation.

By 2025, stablecoins had moved from fringe remittance experiments into the product roadmaps of major consumer money-transfer providers. Western Union, Euronet, MoneyGram, Majority and Remitly announced stablecoin wallets, on- and off-ramps, disbursement capabilities or integrations into their existing cross-border networks. This is meaningful evidence of institutional adoption, although it measures announced capabilities rather than consumer usage or transfer volume.

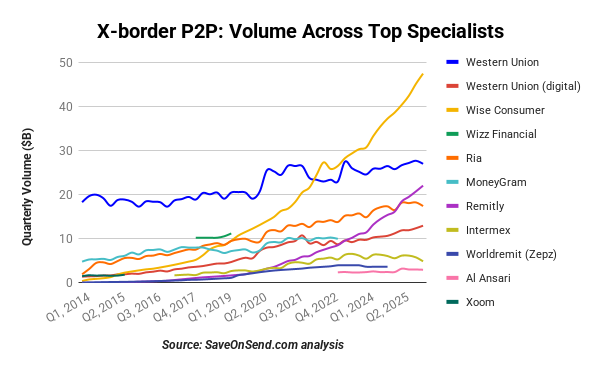

This creates a more revealing contrast than crypto startups versus traditional incumbents. Wise and Remitly became global consumer-remittance leaders by improving the complete P2P proposition: digital customer acquisition, bank funding, compliance, FX, risk management, and local payout. They reached that scale before adding stablecoins, if they added them at all. Stablecoins are now entering some of these networks as an additional back-end rail, but none of the providers in the preceding chart has disclosed how much consumer volume uses that rail or whether it reduces the customer’s total fee and FX markup.

Innovation Adoption: 3 Cases

Stablecoins do not need to replace every remittance rail to become material. They need to win decisively in at least one of three ways: solve a customer problem incumbents leave unresolved, support a business model incumbents cannot match, or create new transfer demand. The rest of this article tests each path.

For disruption to occur, it only takes one determined startup with a long-term vision spanning two or more decades. The disruptive force of innovation only requires one Amazon for books, one Spotify for music, and one Netflix for entertainment. After over two decades since Xoom’s founding, the first fintech in this space, two fintechs ended up ahead of the pack. More than a decade of keen observations in this fiercely competitive space has given us a reasonable understanding of what made Wise and Remitly so far ahead of others, and why some fintechs are no longer around.

“… long, sorry decline has left the 140-year-old company a shell of its former self. Today, it is fighting for its very survival. Western Union fell victim to technological advances…”

Reading current reporting on Western Union’s role in international remittances could lead us to think the company has been a successful monopoly in this space forever. Still, with the arrival of some disruptive innovations (“P2P”, “Bitcoin-stablecoin”, “Social”, “Mobile”,…), there is a real danger of its imminent demise. In reality, Western Union’s subsidiary, Western Union Financial Services Inc., began offering international money transfers in 1982, following deregulation. By the mid-90s, Western Union’s coverage included major remittance destinations, such as China. In those initial years, Western Union (renamed “New Valley” in 1991) experienced numerous upheavals, coming close to or even entering bankruptcy. After changing hands a few times, the money transfer subsidiary was resurrected as an independent entity in 2006. Western Union’s stock performance has been highly volatile ever since, dwarfed by the overall market:

Do remittance startups have a fundamentally different cost structure vs. incumbents? What are the primary customer acquisition channels for money transmitters? What can explain remittance startups’ massively higher relative valuations vs. established providers? If you are interested in such questions, this article is for YOU.

Xoom’s two-decade-plus history is full of missed opportunities and second chances. The child of the so-called “PayPal Mafia” and protege of Sequoia Capital, Xoom was founded in 2001 to disrupt cross-border remittances. At that point, Western Union already had a website where customers could initiate and track money transfers, but it was clunky and saw little use. The shift to online remittances was expected imminently, so creating an online-only provider with a better user experience was a no-brainer.

“Only when the tide goes out do you discover who’s been swimming naked.”

Warren Buffett

Transfast presents a particularly interesting case among providers of international person-to-person remittances. While we often read about startups or bitcoin taking on the industry’s largest players, Western Union and MoneyGram, Transfast was unique in being, till 2019, an acquisition by Mastercard. This independent, private equity-backed company is between those extremes. Transfast straddled mostly offline with some online business worlds across the globe while being nimble enough to maintain an entrepreneurial / startup culture. Between 2008 and 2016, Transfast grew tenfold, expanding from a narrow focus on sending money between the U.S. and Latin American corridors to a truly global provider. Their story and insights on the industry are quite unique and informative.

This blog is specific to Transfast – if you are looking for more general knowledge on the best ways to transfer money, check other SaveOnSend blog posts.

We will cover questions like:

Should I use Transfast to transfer money from the U.S. to India, the Philippines, Mexico, or China?

How do Transfast’s fees and exchange rates compare with other money transfer companies?

How is Transfast different vs. other online remittance providers?

We will structure this post as follows:

Transfast’s history in money transfer

Transfast’s pricing: fees + FX markup (exchange rate)

Whether or not you should use Transfast for money transfer

Transfast CEO’s views on the money transfer industry and current trends

Advertising Disclosure: SaveOnSend.com is an independent, advertising-supported comparison service. SaveOnSend may be compensated in exchange for featured placement of certain sponsored products and services, or your clicking on links posted on this website.

Recent Comments