Do Crypto and Stablecoins Improve International Money Transfers? Evidence from 15 Years of Consumer, Business and Wholesale Payments

“I think we will know when bitcoin has reached prime time when it is transferring more value each day than Western Union or Money Gram…”

Roger Ver, November 2013

Taxonomy:

- Crypto-native transfer: crypto at both ends.

- Stablecoin sandwich: fiat → stablecoin → fiat.

- Digital-dollar access: buying or holding stablecoins without transferring them internationally.

- Consumer remittance: an individual sends money to another individual.

- Business payment or treasury: companies move working capital, supplier payments, or FX liquidity.

- Wholesale settlement: regulated institutions settle obligations between themselves.

- Blockchain infrastructure: the ledger or messaging layer, regardless of the currency transferred.

Since the publication of “Bitcoin: A Peer-to-Peer Electronic Cash System” in 2008, international money transfers, although constituting a smaller portion of cross-border payments, have emerged as one of the most promising use cases for crypto.

The original thesis was simple: remittance users paid high prices for slow, opaque service, while blockchain could move value almost instantly at negligible rail cost. Crypto founders and investors also framed it as a way to bypass banks and reach underserved recipients. Startups raised capital to test that thesis through consumer services and MTO partnerships. El Salvador later turned it into a national experiment by making Bitcoin legal tender and promoting it for remittances.

After more than a decade of pilots, crypto has not displaced conventional consumer-remittance rails at meaningful, independently verified scale. Stablecoins have nevertheless become a credible back-end option in selected corridors and a useful instrument for digital-dollar access, treasury mobility and some high-friction cross-border flows. Most disclosed consumer-remittance implementations remain selective routes, subsidized programs or company-reported deployments whose scale and unit economics are not independently verifiable.

The decisive question is therefore where the full end-to-end system, including funding, FX, compliance, liquidity, payout, cash-out, support, fraud and reversibility, beats modern fiat alternatives on price, speed, reliability and scale. Public evidence remains strongest for digital-dollar access and some business or treasury use cases, and weakest for broad consumer-remittance transformation.

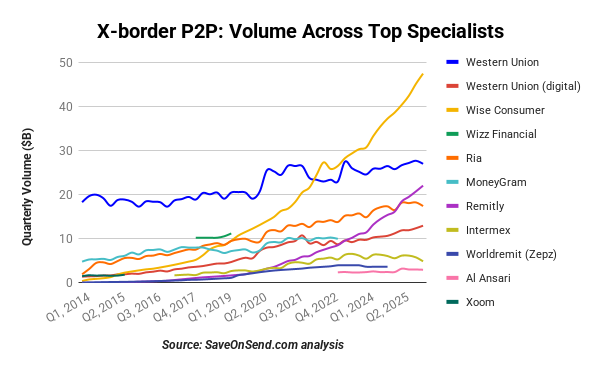

By 2025, stablecoins had moved from fringe remittance experiments into the product roadmaps of major consumer money-transfer providers. Western Union, Euronet, MoneyGram, Majority and Remitly announced stablecoin wallets, on- and off-ramps, disbursement capabilities or integrations into their existing cross-border networks. This is meaningful evidence of institutional adoption, although it measures announced capabilities rather than consumer usage or transfer volume.

This creates a more revealing contrast than crypto startups versus traditional incumbents. Wise and Remitly became global consumer-remittance leaders by improving the complete P2P proposition: digital customer acquisition, bank funding, compliance, FX, risk management, and local payout. They reached that scale before adding stablecoins, if they added them at all. Stablecoins are now entering some of these networks as an additional back-end rail, but none of the providers in the preceding chart has disclosed how much consumer volume uses that rail or whether it reduces the customer’s total fee and FX markup.

Innovation Adoption: 3 Cases

Stablecoins do not need to replace every remittance rail to become material. They need to win decisively in at least one of three ways: solve a customer problem incumbents leave unresolved, support a business model incumbents cannot match, or create new transfer demand. The rest of this article tests each path.

Recent Comments