“The end may justify the means as long as there is something that justifies the end.”

Leon Trotsky, Their Morals and Ours

So you built a mobile app for international money transfer, got seed funding, engaged a few hundred early adopters, and are now ready to go after those outdated, bureaucratic, price-gouging incumbents. How hard could it be? But a year goes by, and your cumulative revenue has barely scratched $100K. The dream of new office digs and sharing a success story with schoolmates is being delayed, while investors are becoming more inquisitive about the timing of the “hockey stick,” all because those strange migrants keep clinging to their existing providers.

Well, don’t fret, we have gathered 5 “best practices” for nudging those close-minded consumers to embrace your service. Most of the cool FinTech kids are doing this and even some incumbents and banks sample them at times, so it must be perfectly legal and not too immoral… at any rate, it is for consumers’ own good, right?

Talking points

Remember that by repeating something, again and again, it will eventually become true. Even if you don’t feel comfortable saying something without evidence, please keep in mind that integrity doesn’t pay for your kids’ private school or a fun team outing. Focus on growth at all costs because that is how everybody succeeds. To get started, tell your Marketing/PR lead to include this top-10 list in all communications going forward:

- Fintech offers 5–10x lower rates than incumbents that charge 10-20% fees

- Market size is $2-5 trillion

- Consumers are naive and are being taken advantage of by incumbents

- Bitcoin/blockchain will be a game-changer for remittances

- There is a fundamental difference in the operating models of Fintech providers vs. the digital arms of incumbents

- Only Fintech/blockchain startups care deeply about the underbanked

- P2P is a game-changer for remittances

- Western Union is about to collapse

- Soon, cash agents will be gone, and digital will reign supreme

Done? Now, let’s apply more sophisticated techniques.

1. Discrediting competition

This technique works well because of its double advantage: consumers not only learn something negative about your competitors but also subconsciously assume that your startup must be pretty good in that dimension. How can a regular person suspect that you have enough guts or legal cover to badmouth competitors for something where you are not much better?

Learn how to get this done – here is TransferWise in an interview with the BBC:

“… independent money transfer giants such as Western Union and MoneyGram, charge about 5-8% in fees when transferring money abroad, and these fees are often concealed within the exchange rate.”

In one sentence, TransferWise masterfully combines 3 negatives about incumbents: they are hulking, expensive, and sneaky! Here is another of their PR mantras in this article:

“…Western Union and MoneyGram, known to take as much as 20% of individual transfers… (later)… it is literally is about food on the table, so there’s an even deeper moral problem to address”

Now, you might have a fresh college graduate on your marketing team who sheepishly suggests that all these statements are false: the remittance industry is highly fragmented, incumbents’ fees in the online space are much lower, and any pricing information is shared upfront. Ignore it – such naive souls typically come around or leave soon, and the allure of FinTech is strong enough to send plenty of eager employees your way.

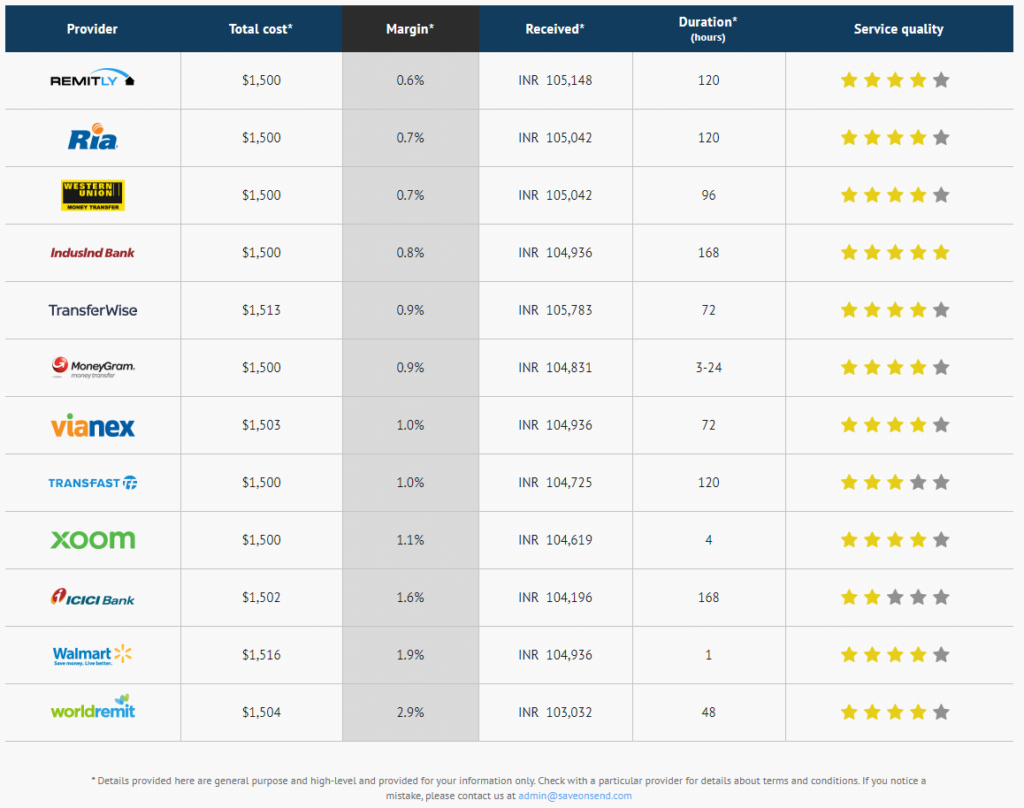

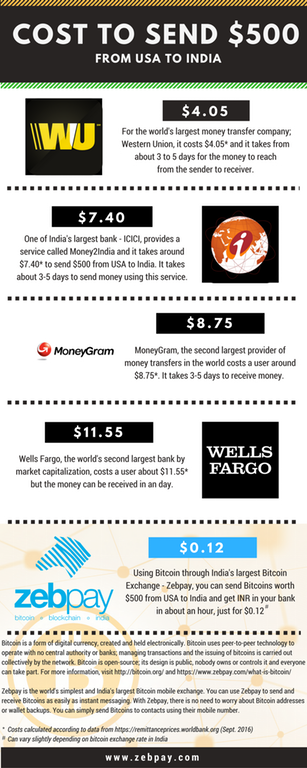

TransferWise is considered one of the most successful FinTech startups – do they get concerned about so-called “facts?” Look at the table below for a typical send amount in one of the world’s top corridors, USA-to-India:

So TransferWise was much more expensive than incumbents. Now, look at this snapshot from its landing page at the time:

Some fact-checkers might complain that TransferWise “conceals” that its margins could be much higher than “0.5%,” but those types of folks are unlikely to be your potential customers. Transferwise’s $116 million in fundraising could be the market’s way of saying, “Onwards with whatever works!”

WorldRemit, another FinTech darling, also doesn’t shy away from this popular technique – here is what it declares in June 2015, years after Western Union, Xoom, and other players launched their digital services, in this article:

“Until now, the U.S. remittance sector has ill-served customers sending money back to many parts of the world…”

The fact that WorldRemit was among the more expensive providers didn’t stop it from positioning itself as a long-awaited savior. Why should your PR strategy be any different?

But why should WorldRemit worry about accuracy when its growth and valuation are so far behind everyone’s favorite TransferWise? Instead, let’s build on stereotypes about backward incumbents (see full article here):

“These are companies that have been operating in the same way for the last 30 years”

“… Western Union is their main competitor at the moment. They have got the legacy, the brand, and the experience, but its lethargic adaptation to new fintech is allowing WorldRemit to progressively bite more and more off its plate”

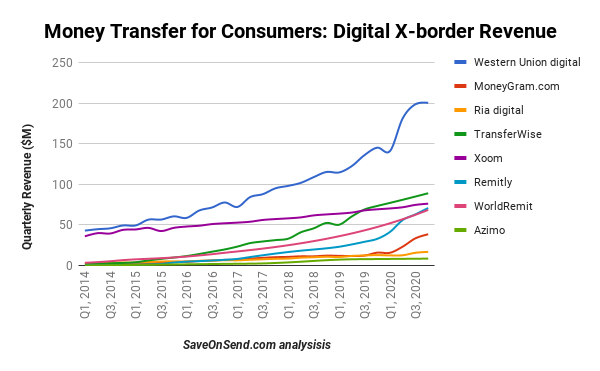

Reviewing the so-called “facts,” one might notice that Western Union’s digital arm has been growing much faster in absolute terms, expanding the gap with WorldRemit from $0.2B to $0.5B in annual revenue over the last 7 years. Hopefully, WorldRemit’s investors are lethargic enough to miss it:

2. Disinformation

This might sound bad, but you are not completely lying in this case. You are only knowingly presenting a fact which is not really applicable… but it is still a fact. For example, what is a silly way to define the market size of international money transfers across consumers? If you responded that the market size of this industry is the sum of all players’ revenues, it would be $30-40 billion, and you might be technically correct.

However, that’s about the same size as the Coca-Cola company, and how many industry “experts” know the definition of “revenues?” Instead, you should use a cooler way to measure your market, by transfer volumes. Learn your talking points from the best:

“…saw an opportunity four years ago to disrupt the $600 billion remittance industry.”

Azimo

“The $550 billion global remittance market is undergoing significant disruption…”

WorldRemit investor

So the market is HUUGE, but you might already know that margins are so-so. What would be a naive way to describe this chart below?

You might be thinking of sharing the latest data point for Global-Weighted Average and, even more unnecessarily, honestly mentioning that the margins have been declining for a while, and then, coincidentally, with the arrival of Fintech startups, the decline has stopped. But what would you gain from such an approach, except informing potential customers that they might not be ripped off by incumbents? Instead, learn how Stellar, whose mission is “to expand financial access and literacy worldwide,” does it in this article:

“A typical transfer can cost 10% of the total remittance; when you’re living on $2 a day that lost $0.20 is a direct cut to basic needs like food, healthcare, and education.”

Impressed? Not just using a decade-old data point, Stellar bravely doubles down, accusing top providers of endangering recipients’ livelihoods and futures. If nonprofit Stellar, with the mission focused on literacy, can act like this, who are you to contemplate a higher moral ground? Reviewing the marketing materials of other Bitcoin/blockchain remittance startups, they have a reputation as do-gooders who want to help poor people and make the world a better place. However, they also need to raise money; hence, repeating the “10-20% fees” mantra seems unavoidable.

Imagine being hired by the likes of Ripple or Libra, supposedly to help the victims of the unbanked menace. Once inside, you realize that do-gooding is just a PR cover for, hopefully, ignorant or corrupt oversight bodies, while your company is printing crypto in the basement. Would you quit like some ethical wimp? Of course not, you realize that real solutions for the unbanked are complex, while the rent in cool places is high today, so you proceed with conviction. Learn from your executives at Libra and Ripple how it is done:

Or let’s say you ordered research, asking a couple of thousand consumers lots of questions in hopes of getting answers to your advantage. Instead, you got something pretty balanced, like “83% of people felt it would be unfair if their [bank] did not inform them of all the costs involved…” Replace “bank” with “provider” or “TransferWise” in the same research, and you would get the same result. But try harder – here is how TransferWise takes this trivial survey response and turns it into a rallying cry in this PR campaign:

“It’s deeply unfair for banks to advertise foreign exchange as free to consumers when in fact they just hide their fee in the mark-up they add to the exchange rate… Customers just want to know what they’re getting – surely that’s not too much to ask? That’s why we are asking the Government to deliver on its pledge to stop misleading pricing in foreign exchange before 2016.”

Surveys are really a goldmine for manipulating understanding public opinion. Make sure they are part of your marketing rotation:

3. Apples and Oranges

FinTech remittance players are taking full advantage of this millennia-old manipulation persuasion technique. It compares two incomparable statements, yet almost none of your customers would know the details of the remittance industry. See how Remitly applies it in this article:

“… on average, customers pay a 7.9 percent fee to send money internationally, but Remitly’s charges average 2 percent.”

Like many other successful FinTech players, Remitly is applying an advanced communication approach that uses two consumer nudging techniques simultaneously: “Disinformation” and “Apples and Oranges.” Using an arithmetic average rather than a weighted average across all remittance-sending methods and comparing it with pricing for its digital-only send method, Remitly looks 4 times better than a typical provider. The real comparison would have been much less appealing:

The unfortunate fact is that Remitly is much more expensive than one incumbent, about the exact cost as another, and cheaper than the last one. Sharing such information with potential customers might be the right thing to do, but it would likely lead to a tense phone call with a junior member of your VC team. You have enough stress as-is, right?

Besides, almost every FinTech remittance startup is doing this. Look at Azimo in this article, boldly comparing its digital pricing with some random high number for Western Union:

“They estimate it generally costs about 2% as compared to Western Union’s 9%.”

Well, let’s compare two snapshots below, taken at the same time for the same transaction. Guess which one is Azimo and which is Western Union:

Does it matter that Western Union’s digital pricing is on par with Azimo’s or sometimes even lower? If you are valuing truth about fame & fortune – maybe, but then why are you reading this article? And stop looking for truth among this season’s disruptive technologies like Bitcoin and blockchain. Their founders are also regular humans who dream of owning a Bentley one day soon, so they really don’t have a choice but to get with a program. Look how quickly these kids are learning:

4. Anchoring

This is a popular negotiating technique which could be also applied for confusing guiding consumers. The idea is to come up with a meaningless but impressively sounding yardstick that superficially differentiates your startup from competitors. Let’s look at its practical application by WorldRemit in this article

“The company is also differentiating itself from its competitors by existing entirely online.”

Considering that every incumbent has a digital unit that provides online services, this sentence seems odd, but many consumers might not know this and could believe their current provider is behind the times.

Incumbents themselves are eager students of this technique. Here is how Western Union does it:

While “zero fees” is an irrelevant data point, since Western Union is charging an FX markup, most consumers would perceive it as an indicator of very low prices. Many SaveOnSend readers were surprised to find out that their favorite provider, like Western Union or Xoom, is actually making good money from them on the FX markup – such was the strong effect of “zero-fee” propaganda. Banks also refuse to give up on misleading consumers by actively PRing “no fees” as the real benefit:

But of course, it takes the passion of a Fintech startup to take this technique to a whole new level. Rather than playing with piecemeal marketing, they dare to build the entire company around this anchor. Of course, they charge users a comfortable FX markup, but wouldn’t customers feel better if they thought that they were getting services for free? TransferZero’s evident response is “Hell Yeah”:

“…we, care about our consumers and their needs. We try to approach take the most of the technology for customers and their loved ones. TransferZero is the first Spanish Remittance Fintech 100% online, the service provided is easy, fast, secure and FREE!”

Xoom is teaching us another way to apply the “Anchoring” technique. In July 2015, Xoom began publishing this ad for the USA-to-India corridor:

To unpack this a bit, a provider’s exchange rate depends on a) the interbank exchange rate and b) the provider’s FX markup. The higher the (a) and the lower the (b), the better the provider’s exchange rate is. Let’s now look at Xoom’s exchange rate, dollar-into-rupees, during this period:

Let’s now compare it with the interbank exchange rates during the same period:

Both graphs have almost the same shape, yet Xoom still proclaimed “best rates ever!”, making its customers feel the company had something to do with it.

Xoom is also a master at emotional anchoring. They remind us every time how deeply they care about poor consumers without access to banking services, also known as “unbanked”:

Does it matter that they provide no services for those consumers? Obviously not. Who has time for a detailed analysis of their segment and product strategy when their message reassures everyone that someone is taking care of those poor folks in Africa? So keep your PR anchoring on an emotional connection to humanity while your colleagues take care of well-off folk with $2,000+ transfers. Learn from the pros on how to talk about the unbanked as if you really cared:

5. Lying

This is a tough one. While most of FinTech stars are comfortably applying Techniques 1 through 4, very few are ambitious enough to make a blank false statement.

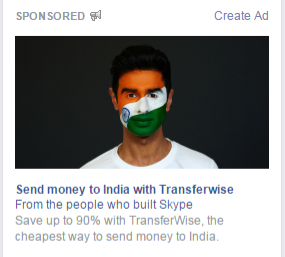

As often, TransferWise, such a rebel, sets an example of goal orientation. As you remember, for the USA-to-India corridor, TransferWise is one of the most expensive providers. How does #8 among global disruptors handle it? With gusto:

TransferWise: Facebook Ad, April 16, 2015

Not only does TransferWise promise 90% savings, it claims to be “the cheapest” provider. Considering that TransferWise is outperforming other FinTech startups, sped past Xoom, and caught up to MoneyGram, can you really afford not to follow its approach in every detail?

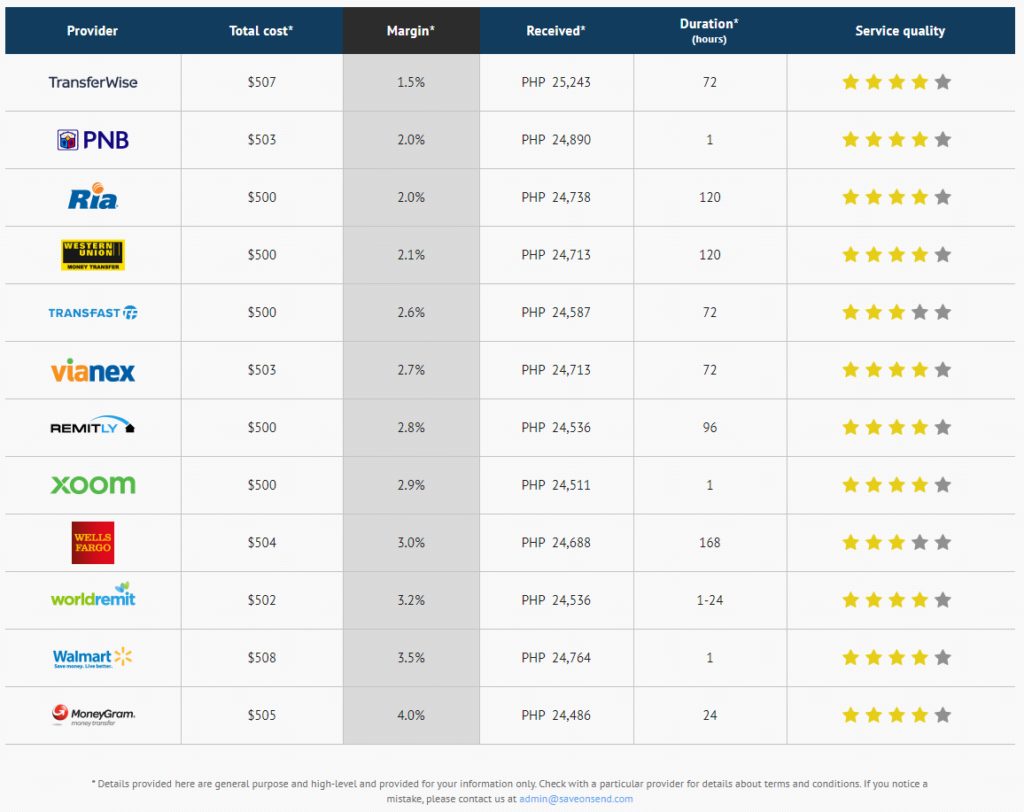

Other fintechs followed this courageous technique. Remitly really wants to grow fast, so its capable team even came up with an interesting twist on a first-time-customer promotion, offering a very favorable exchange rate, sometimes above interbank:

Not bad, but how would you make the most of this one-time promotion if lying is ok? With Forbes help, Remitly claimed that it is actually their standard pricing:

Remember why you got started in the first place: probably wanted to help some people, make the world a better place… but what if it means fewer bragging rights? The balance between money, fame, and integrity is always up to you.

In Conclusion

If you feel that our article is biased in any way and/or doesn’t mention other providers that use the same techniques, please provide proof in the comments section below. We will gladly rectify any inadvertent omission.

If you are a customer of these providers and feel misled, please share your experience in the comments section below. You are also welcome to contact the appropriate government agencies in your country. For example, in the USA, it is the FCC and the CFPB.