“I think we will know when bitcoin has reached prime time when it is transferring more value each day than Western Union or Money Gram…”

Roger Ver, November 2013

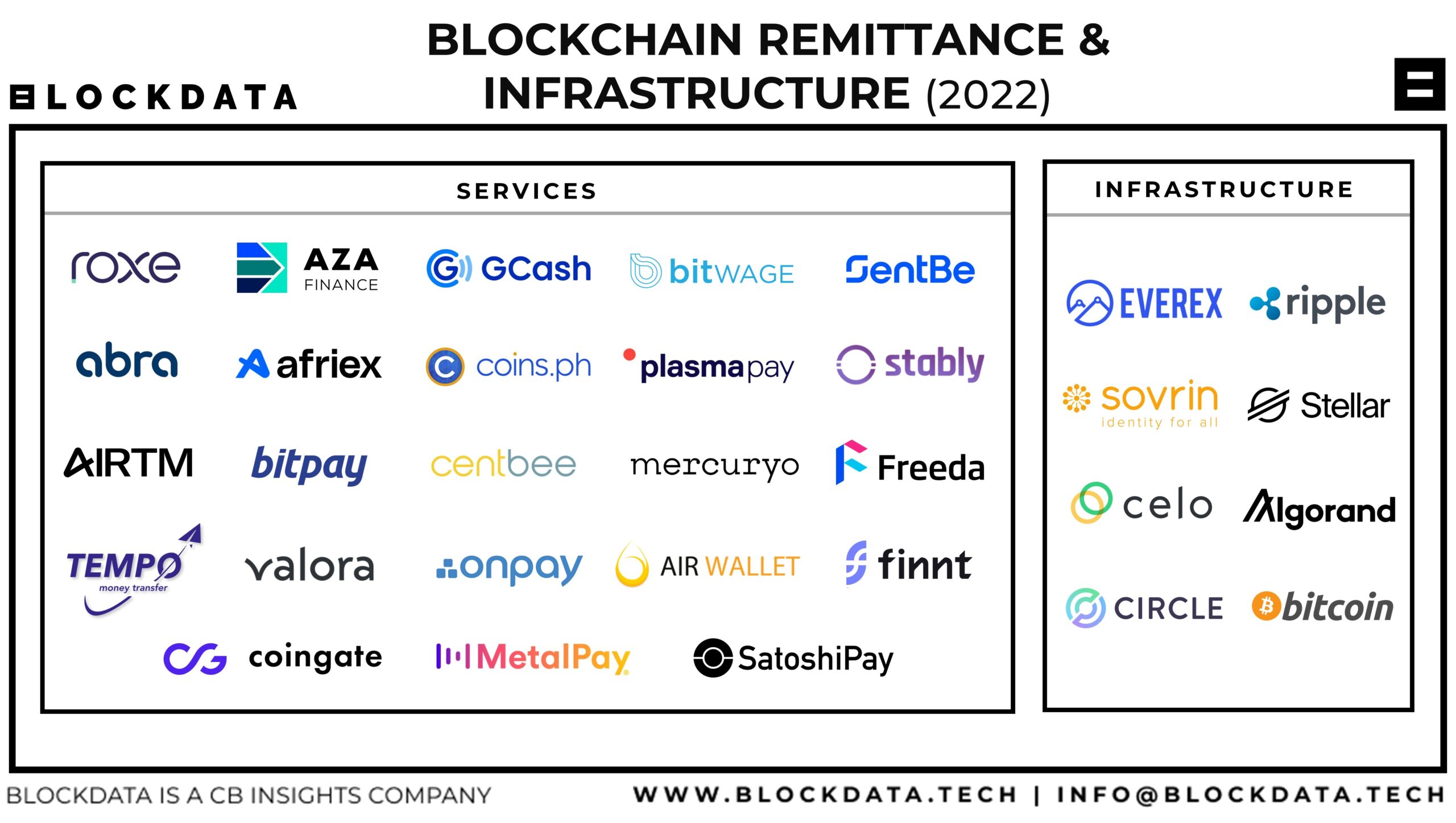

Since the publication of “Bitcoin: A Peer-to-Peer Electronic Cash System” in 2008, international money transfers, although constituting a smaller portion of cross-border payments, have emerged as one of the most promising use cases for crypto.

The initial assumption was that remittance users were experiencing exorbitant fees and subpar services from traditional players like Western Union. The prospect of an almost cost-free and instantaneous blockchain-based solution appeared to be a much-needed relief. Additionally, it presented an opportunity for affluent individuals in Western countries to showcase their efforts toward promoting financial inclusion in developing nations.

Subsequently, many startups received funding to test this hypothesis with consumers and partner with money transfer operators (MTOs). Additionally, one country recognized this as a national priority and encouraged its citizens to explore cryptocurrency-based remittances.

Despite this, the adoption of cryptocurrencies for remittances has not increased in the last decade. Using crypto for international money transfers remains a pilot or pay-per-play. More importantly, nobody can articulate an in-depth case for using private, public, or government crypto instead of or on top of Swift + local real-time rails.

In contrast, non-crypto fintechs such as Wise and Remitly have emerged among the global leaders. What factors have contributed to the disappointing start for crypto, and will this innovative technology have a more significant impact in the future?

Innovation Adoption: 3 Cases

Consumers and businesses possess trillions of dollars of disposable income that they eagerly spend on various products and services, regardless of whether they are beneficial. For instance, consumers collectively spend around a trillion dollars annually on alcohol, junk food, or tobacco. Introducing genuinely innovative technology is an even more straightforward proposition. Financial services and insurance companies allocate a trillion dollars annually to technology spending alone. Apple generates $200 billion just from iPhone sales. While generative AI is still in the early phase, Nvidia’s annual sales of AI chips have already reached $150 billion. To achieve similar success, blockchain technology only needs to address one of the three following use cases:

- Incumbents fail to address customer pain points (Blockbuster -> Netflix).

- Incumbents lack a scalable business model (Borders -> Amazon).

- Technology spawns entirely new demand (radio -> Spotify).

Is a significant segment of money transfer users suffering without crypto?

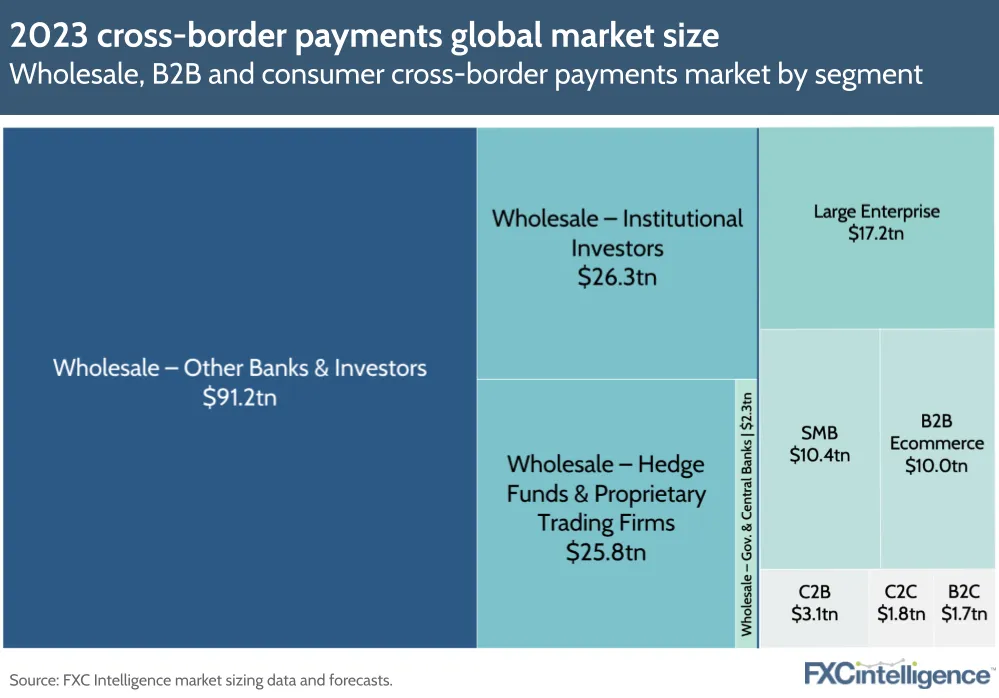

Articles titled “The Unexpected Tragedy Of The Financial System” have been prevalent for the past decade. These virtue-signaling stories often promote crypto to help the poor in developing markets but lack field research or customer surveys. Consumers pay around $60 billion annually to money transfer providers for remittances and C2B use cases like education. Remittances account for about half of that amount, and it would be neat to figure out a way to provide the same service while the industry is earning much less.

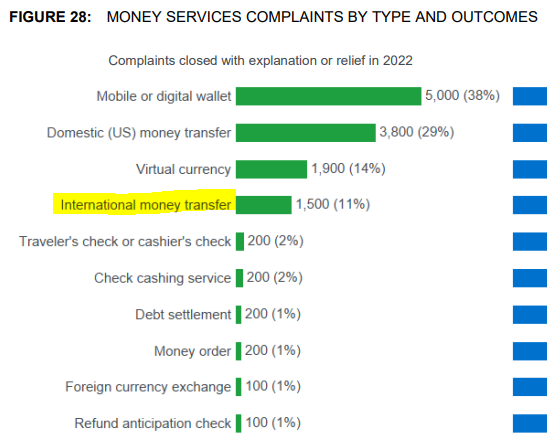

The question remains: Are consumers genuinely dissatisfied with their current cross-border money transfer providers? In 2022, a US government agency responsible for consumer financial protection received only 1,500 complaints, despite a billion transactions totaling $200 billion in cross-border money transfers. Interestingly, the agency received 25% more complaints about virtual currencies during the same period, even though their adoption was much smaller.

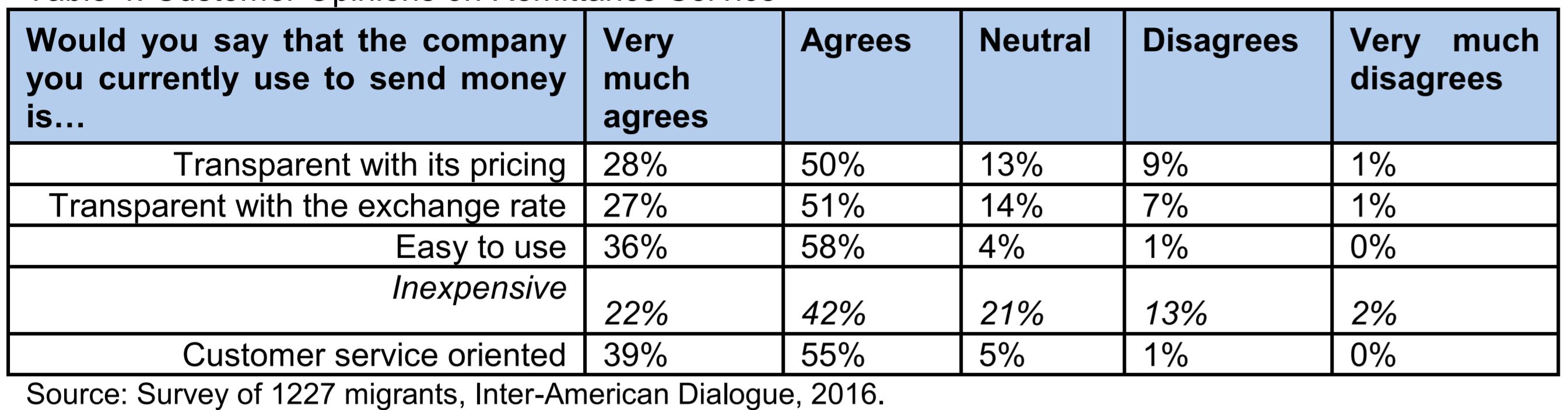

Engaging in conversations with a sufficient number of low-income consumers who conduct international money transfers would reveal that there is no “tragedy” as often portrayed. Even more perplexing, this segment doesn’t seem motivated to save on money transfers. In a 2016 survey, even before the fintech-driven price decline, only 15% of migrants believed their current provider was expensive.

The reluctance of low-income senders to save money on international transfers is not due to a lack of infrastructure. Over 90% of cash senders possess smartphones, and over 80% have bank accounts that can be readily linked for online money transfers. Despite these options, many still prefer using cash agents, paying 2-3 times more to send money home. The transition from offline to online remittances has progressed by 1-2% annually. It wasn’t until the global pandemic in 2020 that this shift toward digital methods experienced a temporary acceleration (source: Family Remittances 2022 in Numbers):

The gradual shift in payment habits is not exclusive to remittances. Indeed, it has taken decades for consumers to transition from cash to plastic cards, from paper checks to online billing, or from the traditional “swipe-insert” plastic card to the modern “touch” payment methods using smartphones or smartwatches. The consistent underlying reason for these slow transitions is that consumers do not perceive any issues with their traditional payment methods.

Can crypto money transfers help the needy?

Crypto- or fiat-based fintechs focusing on money transfers often use narratives involving “unbanked,” “poor,” or “women” recipients of remittances in developing countries as their inception story. Consider the scenario of a hunger-stricken woman with no financial accounts in a sub-Saharan village. We are asked to believe that the founders are losing sleep trying to find a way to improve her situation by using their digital remittance solution. Like the stories about the challenges faced by remittance senders, it’s pretty likely these startup founders have never encountered such a person. Their claims often lack specificity regarding how to target such segments and an explanation of the viability of generating revenue through such challenging targeting.

The argument that crypto remittances help unbanked consumers contains misconceptions about the sending and receiving ends of a money transfer. As we previously discussed, most senders have both a bank account and a smartphone and are generally content with their experience of sending cash. However, the question arises: Why do they choose to send cash? Many consumers opt for cash transfers in specific corridors to avoid potential deportation and taxation issues. Luckily for them, since Western governments often face challenges in managing seasonal migrant labor, financial regulators adopt more lenient identification standards for individuals sending smaller amounts (under $3,000) cross-border in cash compared to digital channels.

Here’s how the CEO of a major traditional provider described this challenge:

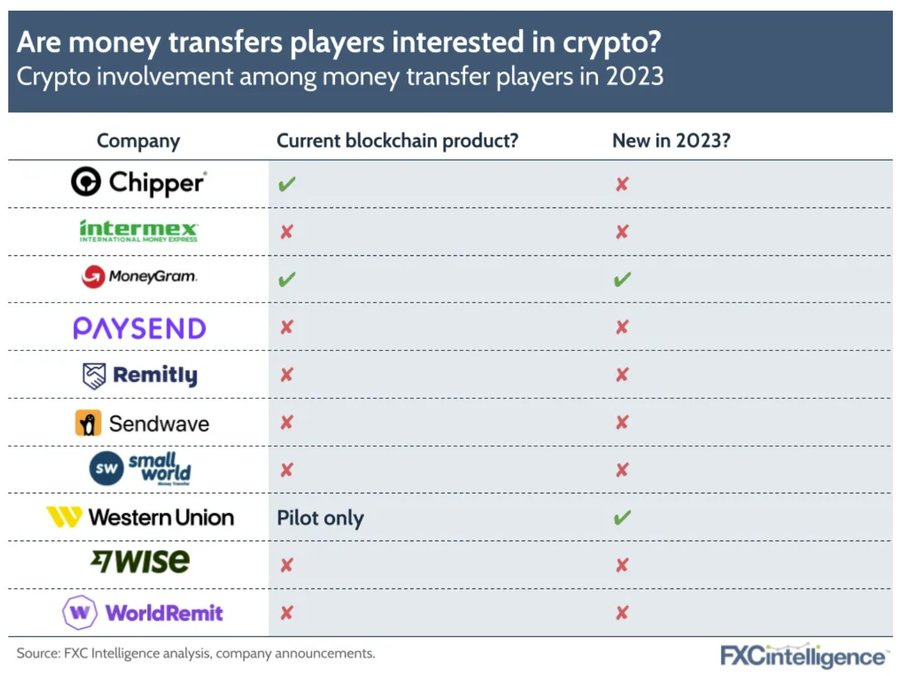

Crypto-based money transfer firms could theoretically help these people with an anonymous solution, but that would be illegal. Meanwhile, starting in 2023, several well-funded fintechs have begun targeting this segment with less stringent identification requirements (Alza, Majority, Maza). By 2025, Alza and Majority were shut down, and Maza was acquired.

Fintech companies operating in the largest developing countries, such as China and India, have had an even more significant impact on banking unbanked consumers. Startups like Alipay, WeChat Pay, and Paytm have successfully brought hundreds of millions of previously unbanked consumers into the digital financial ecosystem, enabling them to receive money and make digital payments.

Another significant driver of banking the unbanked arises from the governments of developing countries that are implementing real-time payment systems with payment accounts for their citizens. Examples include India’s UPI and Brazil’s Pix, which have brought tens of millions of previously unbanked citizens into the financial fold in recent years.

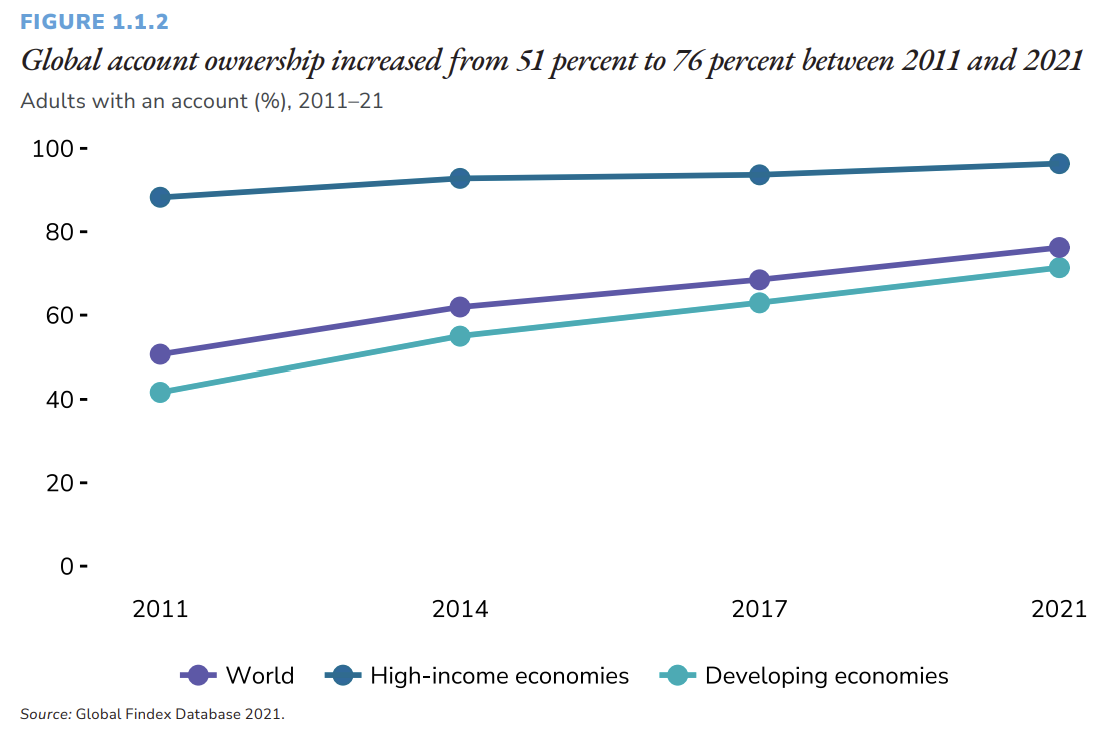

As a result, the number of unbanked individuals has been rapidly decreasing, from 2.5 billion in 2011 to 1.4 billion in 2021, even amidst a significant global population increase of approximately one billion during that decade. With this trajectory, it’s conceivable that the developing world could reach a level of financial inclusion comparable to that of developed economies by 2050.

However, it does not pose a significant inconvenience or cost issue even for the remaining unbanked consumers on the receiving end of remittances. With approximately half a million Western Union agent locations, along with a similar count for Ria and MoneyGram, money can be easily collected by the vast majority of unbanked recipients. There is so much capacity that around 30% of these locations experience no remittance activity. While there will always be pockets of consumers residing in highly remote areas, reaching them electronically in a cost-effective manner would necessitate expensive technologies similar to Starlink.

Unbanked consumers are not significantly disadvantaged in pricing since the sender covers all the fees. Moreover, receiving money digitally is only slightly less expensive, typically costing around 1% of the transaction amount for a typical transfer.

Unbanked consumers could receive money instantly for the last two decades, albeit it might cost a sender a bit more. As developing countries have introduced real-time payment rails, money transfer incumbents and fintechs are quickly plugging their networks into those new rails, delivering money instantly across the globe.

Many early crypto remittance startups were established before 2015 by individuals without significant cross-border expertise who were unaware of these facts. They held a genuine hope of assisting the unbanked with remittances. In contrast, founders of blockchain-based startups that emerged after 2016 typically came from the industry and were well aware of this information. Nonetheless, they still repeat the same pitch of aiding the “2 billion unbanked” while targeting digitally savvy, more affluent consumers.

There is good news for crypto enthusiasts who genuinely embraced this novel technology to alleviate the suffering of the poor, unbanked, women, and other marginalized groups. Don’t be disheartened by the lack of crypto adoption by these individuals. Even if the crypto ecosystem were to disappear tomorrow, traditional technologies and methods have a proven track record of effectively addressing poverty and fulfilling the financial needs of these marginalized populations.

Bitcoin/Crypto/Blockchain money transfer is instant and, thus, doesn’t carry the FX volatility

The “nearly-instant-free” transfer via Bitcoin was valid to some extent up until the middle of 2015, but the Bitcoin community was unable to solve a technical problem that led to systematic transfer delays and higher fees (see details here). However, Blockchain proponents associated with the likes of Coinbase and Ripple like to make misleading or ignorant statements about traditional fiat-based players providing an inferior service. They often point to the enormous time lag for sending money using traditional methods. Here is an idiotic explanation from the interview with Ripple’s executive in October 2019:

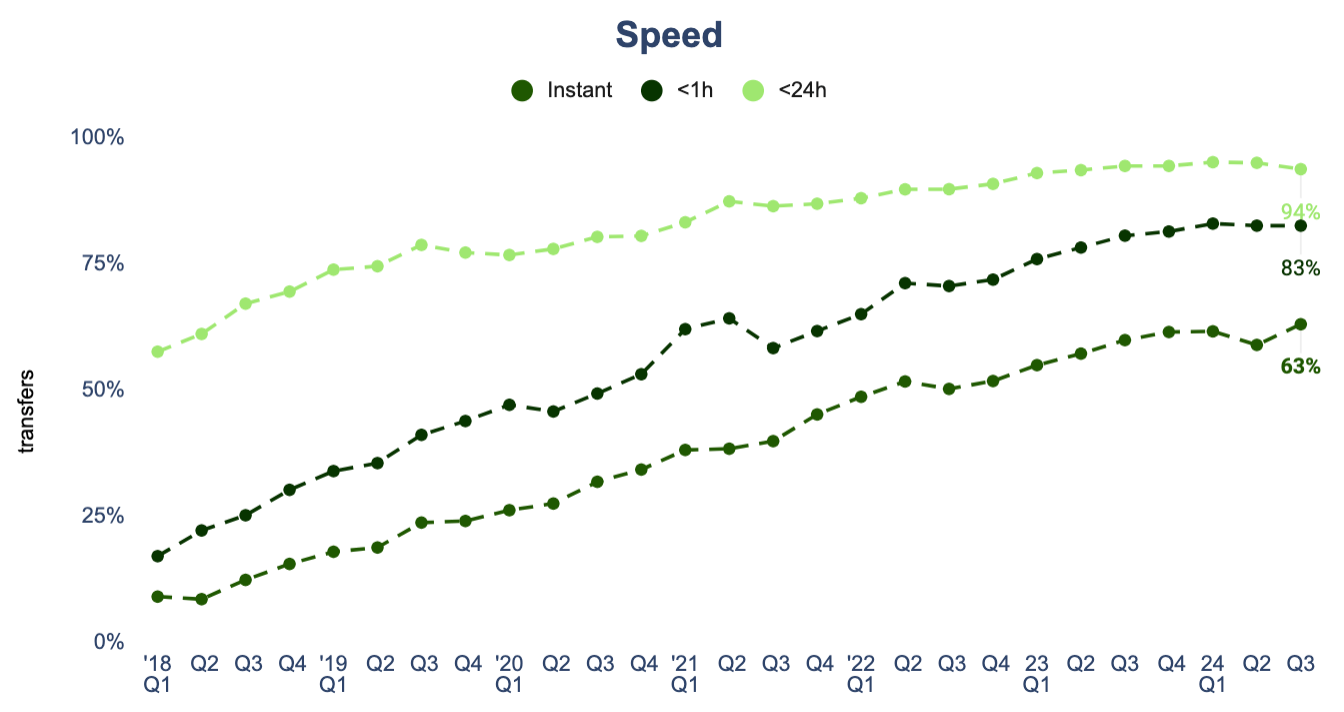

In reality, starting in the late 90s, all major money transfer providers offered minutes-long transfers. Since the mid-2000s, Xoom has been offering the same transfer speed digitally. By 2024, Wise’s (global digital leader of cross-border money transfers) one-day transfers reached 94%, while instant transfers were 63% of all transactions.

By 2023, approximately 80% of all payments on Swift were sent via its modern gpi rail. 40% of gpi payments were credited to end beneficiaries within 5 minutes, while almost 100% of gpi payments were credited within 24 hours.

In the world’s largest corridor, USA-to-Mexico, most of the providers already deliver funds in minutes (see full results at https://limonfinancial.com/envios-dinero/envios-de-dinero-a-mexico/):

Non-crypto money transmitters can send money instantly because they have built strong risk management capabilities and local bank connectivity while pre-funding daily needs. Plus, sending money via a debit card, while costing slightly more, is also instant, as providers see less risk in those transfers. Banks historically had to rely on outdated government networks, which could take a few days to confirm a transfer. However, since the mid-2000s, Australia, the UK, and other countries have implemented near-real-time payment capability. In some countries like the US, there are two local instant rails, banks, and government-owned (RTP and FedNow). Similar implementations in other countries are on the way, with most developed countries expecting to launch near-real-time rails by 2030.

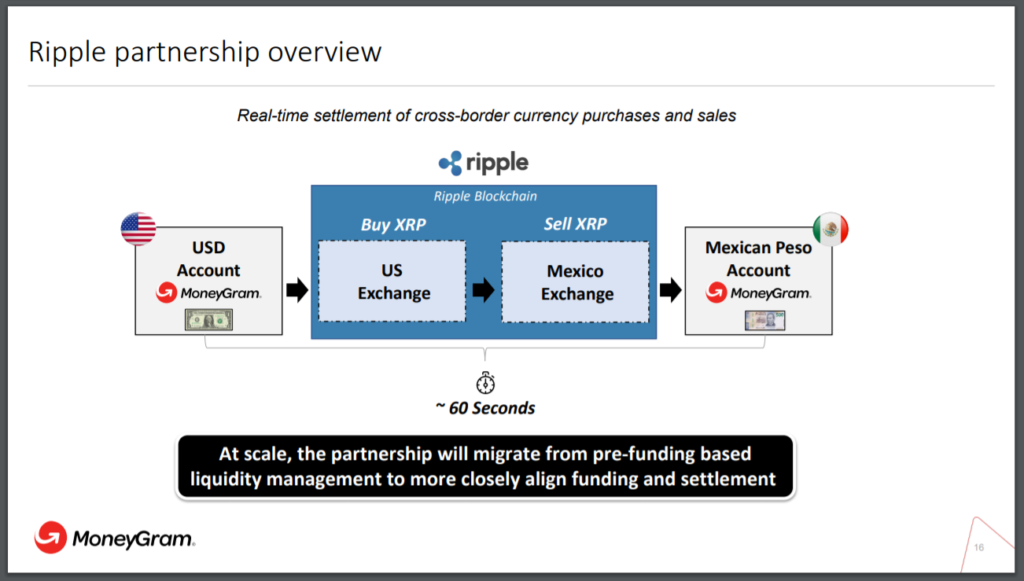

So, any speed advantage of the Bitcoin crypto blockchain has been eliminated. Moreover, a transfer via Bitcoin/crypto/blockchain carries an FX conversion disadvantage, a double whammy. Here is how MoneyGram depicted its use of Ripple/XRP rail during their partnership in 2019-2021:

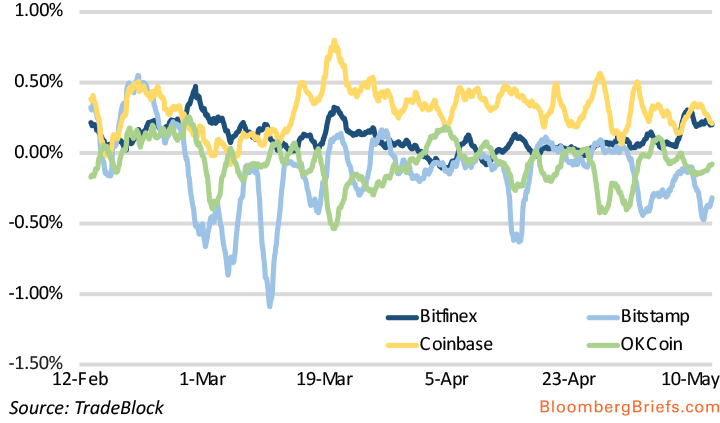

Instead of converting money directly between two highly traded currencies, dollars and pesos, MoneyGram bought and sold out of obscure crypto. Because of XRP’s relatively tiny trading volume, its FX margins were naturally much higher than with fiat currencies, and, again, those margins have to be paid twice. The same higher FX margins are the case for all cryptocurrencies and exchanges:

Here is how HelloBit’s co-founder and CEO, Ali Goss, summarized this conundrum in Bitcoin Magazine in 2015:

“With bitcoin, you’re adding a third currency,” Goss said. “You go from U.S. dollar to bitcoin, and then from bitcoin to whatever the local currency is. You’re adding an extra FX move right there alone. That increases friction. On top of that, small startups don’t have a big FX department, and they don’t have the big abilities that come with such a department … they’re generating more costs for themselves, not less.”

The spreads are so high that even die-hard crypto cross-border players use non-blockchain rails to complete transfers for those destinations. Yes, you heard this right, EVERY so-called Bitcoin/blockchain money transfer startup pays banks to process a large portion, sometimes a majority, of its cross-border transfers. Here is ZipZap in this interview with CoinDesk:

“ZipZap uses a combination of traditional (Swift) bank payment rails and blockchain technologies to find the least expensive and most efficient transfer option…”

But why would MoneyGram use Ripple/XRP and lose money on a more expensive extra FX conversion that it has to perform twice?! More on this later, but in 2019, MoneyGram was desperate for cash, allowing Ripple to buy 10% of the company while paying $40 million annually to create a perception of XRP liquidity in Mexico. Here is how MoneyGram described the partnership to investors:

Therefore, instead of disrupting cross-border players or at least helping them serve the unbanked, crypto/blockchain players are using those firms to prop up their printing presses. Any PR is good if more naive consumers buy a novel cryptocurrency without intrinsic value. Now, you can also begin to appreciate why, during those years, Facebook leadership and their Silicon Valley friends were looking at the Ripple scheme and wanted to join in on the action by launching Libra/Diem.

In 2023, Coinbase still promoted its cross-border money transfers as having no fees to send/receive and instant availability:

Most remittance senders do not initially hold their money in cryptocurrencies, and the users on the receiving end have even less demand for crypto. How did Coinbase facilitate cash-out, and what is the FX markup that receiving customers pay for this service? In this regard, Coinbase partnered with Remitly, one of the most prominent players in digital remittances. Here is how Remitly’s CEO characterized the arrangement in 2022:

Bitcoin/crypto/blockchain can dramatically reduce remittance prices

Most of the potential savings for international money transfers could be realized today, immediately, IF ONLY senders stop going to cash agents and spend 3 minutes linking their bank accounts on their smartphones using their existing providers like Western Union or Ria Money Transfer. Not understanding why so many senders continue spending 2-3 times more while having a bank account and a smartphone will likely lead to many disappointments for the next generations of Bitcoin-crypto-blockchain-based money transfer startups.

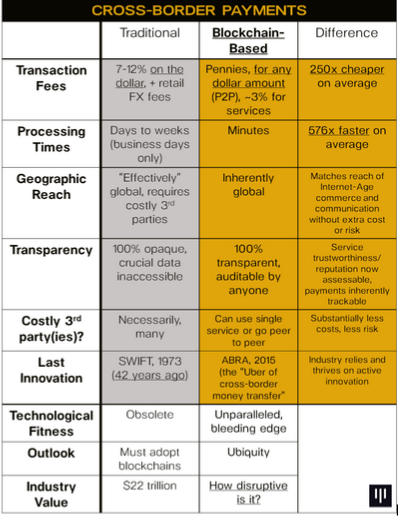

Examples of past disappointments are common- see the “Graveyard” section toward the end of this article, or read these insights from Bitcoin entrepreneurs. But still, too many Bitcoin remittance stakeholders kept repeating an outdated adage about a high markup charged by “traditional” providers and that a Bitcoin solution is 250x cheaper:

Here is another typical comparison from March 2019, highlighting the advantages of free and immediate remittances offered by blockchain startups in contrast to traditional fiat-based firms’ slower and costlier services. However, these articles consistently fail to explain why, despite having such advantages and significant marketing capital, as well as numerous pilot projects with established companies, none of these crypto remittance players have been able to demonstrate impressive transaction volumes, except in cases of partnerships involving paid transactions, such as Ripple with MoneyGram.

Similar claims were made by the short-lived Facebook venture Libra/Diem. After facing challenges in scaling the P2P payments business at Facebook through traditional means, David Marcus, the head of payments, established a blockchain-based company. Recognizing the difficulties of obtaining government permission to issue currency, Libra/Diem sought political cover by asserting that their primary goal was to assist the billions of unbanked individuals with their remittance needs. However, it remains uncertain how much they truly understood about remittances at that stage. Here is what David Marcus said in late 2019:

You judge if such ignorance was unintentional or if Facebook was shamelessly using the world’s poorest to make a quick buck. A similar lack of understanding has been prevalent among Fintech experts. Here was Chris Skinner on a Breaking Banks podcast in 2017 (starts at 32:45):

“Now using companies like Abra a US citizen could send someone in Philippines a hundred dollars with hardly any commission taken off, compared to 25% or more being taken by traditional players.”

How much did that transfer cost at the time? 2-4%:

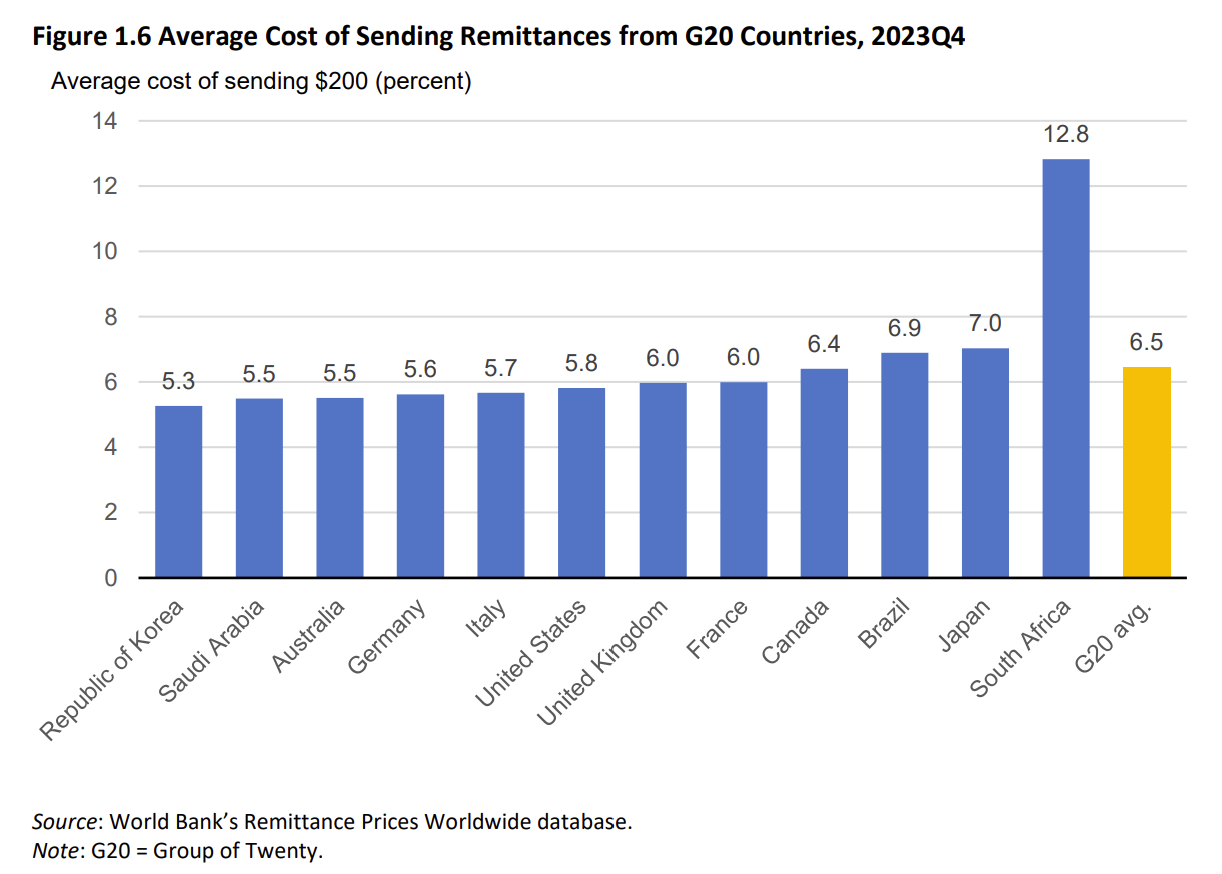

By checking price comparison sites for major remittance corridors, one can quickly discover that top incumbents’ weighted average global margins have been falling closer to 3% among traditional players and even lower for some fintechs.

So, why are we still seeing so many articles about the high costs of sending money internationally? This was the case in the past, and changing our mindset to a fundamentally different input is hard. As usual, high margins attracted more competition, and prices dropped dramatically. For larger amounts, the average global price is below 5%, and for informed consumers, it is 3%:

The average pricing from the world’s largest remittance corridors is generally similar, except in South Africa.

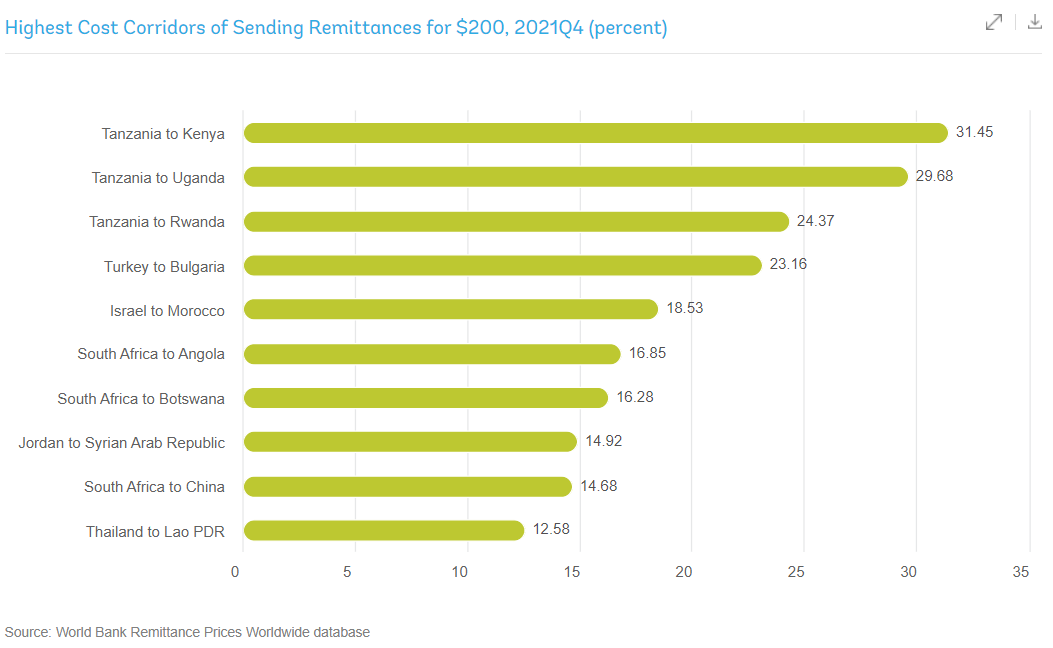

Most of the world’s most expensive corridors originate in South Africa and Tanzania. If Bitcoin-crypto-blockchain startups care so much about the high prices of remittances, do you know why they haven’t opened offices in those countries?

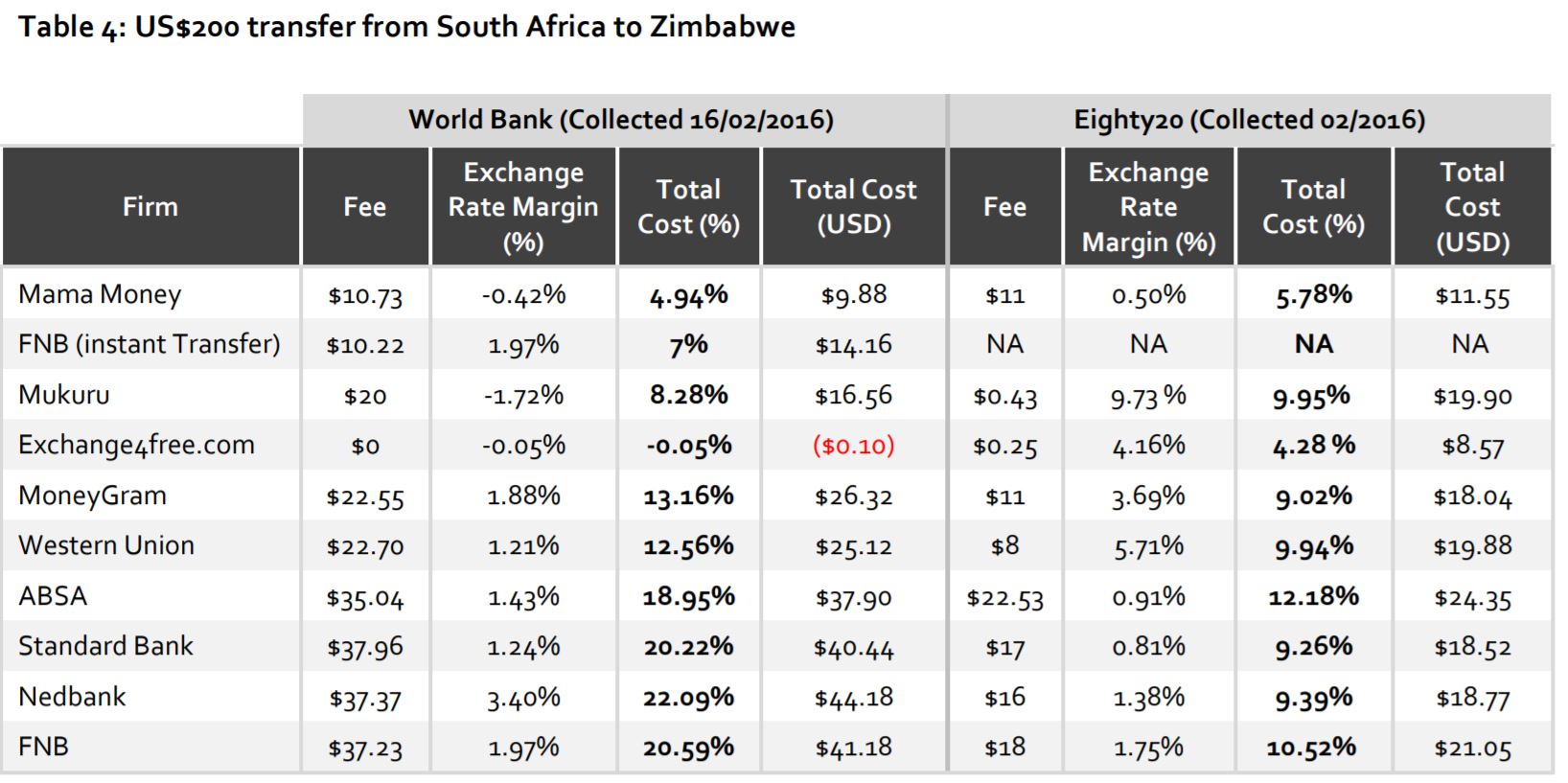

Such data is hard to gather and maintain, so the actual prices might be even lower, as it was discovered in 2016:

What is causing South Africa’s outbound remittance prices to be many times more expensive than those from a country like Russia? Most experts would claim that it is due to two issues: de-risking by banks and exclusive partnerships with retailers by Western Union and MoneyGram.

“A major barrier to reducing remittance costs is de-risking by international banks, when they close the bank accounts of money transfer operators, in order to cope with the high regulatory burden aimed at reducing money laundering and financial crime. This has posed a major challenge to the provision and cost of remittance services to certain regions.”

“… the core issue with WU is their exclusivity clauses that have been used for decades to successfully lock markets to one provider, who can then increase their mark-up fees as there is no alternative.”

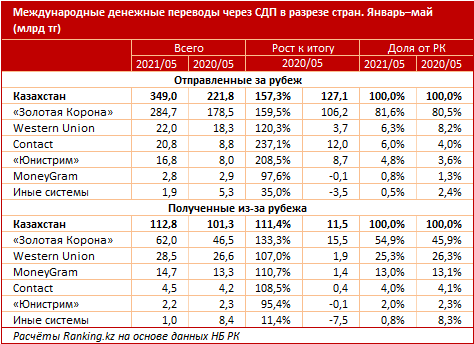

Neither of these reasons is the case. It is easy to blame ‘banks’ or ‘Western Union,’ but the actual root causes are 1) opaque and corrupt governments with regulations that favor banks over Money Transfer Operators (MTOs), 2) consumers who don’t care to shop around, and 3) incumbents who are content with maintaining their market share status quo. In the former Soviet Union region, these constraints don’t exist regarding remittances, resulting in lower margins, with Golden Crown being the market leader across many countries, including Kazakhstan. See the proof in the table below – some company names are in Cyrillic, but you can probably guess their English names, too.

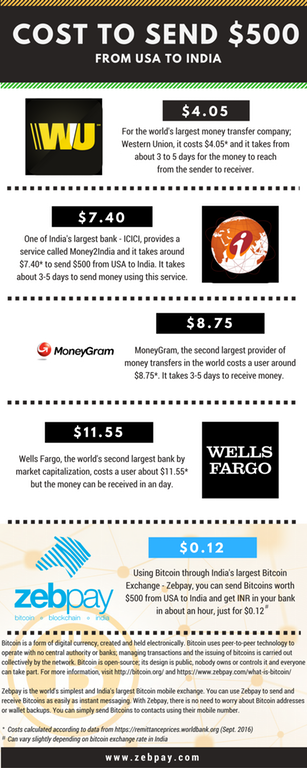

More relevant for Bitcoin/crypto/blockchain-based remittance providers, whose customers tend to be tech-savvy early adopters, the margins for online remittance in top corridors are in the 1-3% range. For example, in the world’s most advanced corridor, USA-to-India, many providers don’t charge any fees for digital transfers, and their FX markups are typically around 0.5-1%:

Let’s review the FX markups for another world’s top-10 corridor, USA-to-China. For 6 months in 2016, Western Union was charging ZERO, no fees or FX markup, for sending money online, from-to the linked bank accounts. In 2019, Ria Money Transfer even had a negative FX markup to its customers, i.e., they were offering customers a higher exchange rate than on the interbank market:

In other words, in some corridors, providers have been subsidizing customers to use their services:

It is true that the digital service from Western Union and Wise is not free and not always instant, so if Blockchain-based providers could offer their services for free AND in real time, they would have an advantage, as long as their investors don’t mind a business model with a negative variable margin.

Some Bitcoin/blockchain remittance startups claimed that they were offering such services:

But hiding behind a small font was a misleading comparison between sending money with a popular, easily verifiable fiat-to-fiat method and a transaction originating in Bitcoin without mentioning a Bitcoin-to-fiat spread. On top of that spread, Bitcoin providers were charging increasingly higher fees (source here):

The fee volatility got so bad that in October 2017, Bitspark, one of the more prominent B2B providers of Bitcoin money transfers, switched away to another blockchain.

Since 90% of remittances are still received in cash, could consumers save money by receiving cash from Bitcoin/crypto ATMs? Nope, it is even more expensive:

As mentioned, some of the world’s largest remittance corridors allow the same currency transfers, such as USD-to-USD from the US to the Philippines or China. This naturally eliminates the need for a provider to manage FX volatility and leads to very attractive pricing for consumers:

On the other end of the spectrum, there are numerous tiny ($1-5 million in annual volume) corridors, especially in intra-Africa, with obviously very little competition and much higher margins. The smaller the corridor, the less likely the return on building localized digital capabilities. That is why the largest digital cross-border money transfer player, Wise, was available from ~30 countries outbound and ~50 countries inbound by 2023. Western Union only enabled digital transfers from less than 40% of its worldwide destinations, 75 outbound countries, by 2020.

But Bitcoin/crypto/blockchain startups are different. Right? Unlike the profit-maximizing Western Union or expat-oriented Wise, these startups were started to help those in need who get overlooked by the large existing providers:

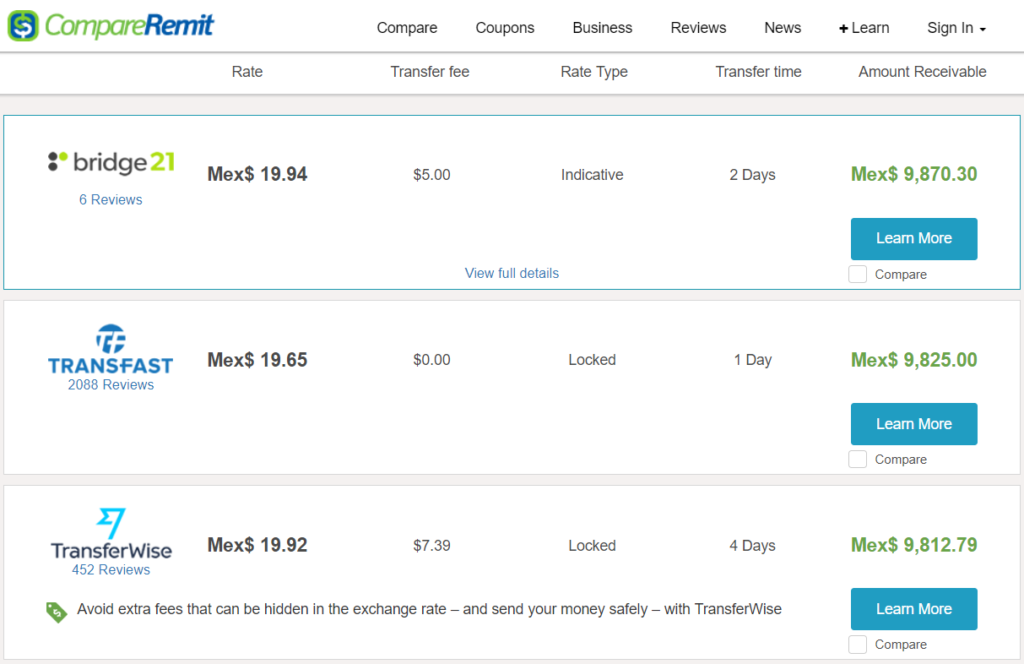

So, which desperate Sub-Saharan Africans did Bridge21 decide to help first? None. Since 2017, the startup has been targeting well-off customers in the world’s largest and one of the most saturated corridors, USA-to-Mexico, where a margin for such service is 1-3%:

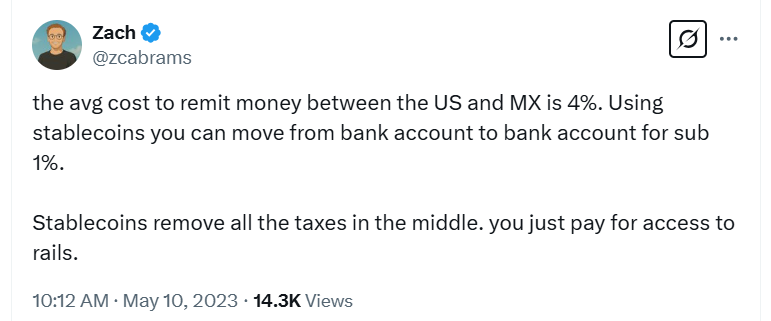

Most of the facts in this article have been well-known since 2016, yet shockingly, every year, new Bitcoin/crypto/blockchain startups emerge that don’t want to understand the difference between a lab experiment in the metaverse and why remittances function in a certain way in the real world. Zach Abrams, co-founder and CEO of the stablecoin payments platform Bridge, conveniently believed that the average cost of remittances in the world’s largest corridor was 4% because fiat rails are bad.

Was Zach interested in learning that Wise and other fintechs charge less than 1%? Of course not. Once you start nitpicking addressable markets, you risk ending up with a mixed bag— and then Stripe might not spend $1.1 billion acquiring your startup.

Quick aside: Mobile Money

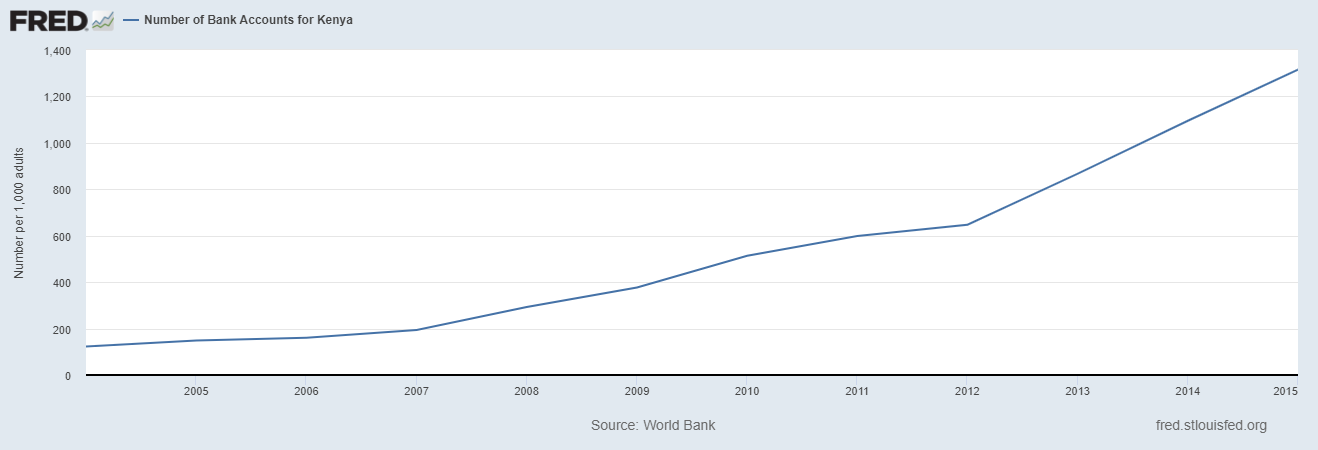

Separate from crypto, there is a narrow case of “mobile money,” which typically implies that money is paid from a customer’s account with their telecom provider. Despite being piloted by Western Union in 2007, mobile money payments remain a tiny portion of global remittances. They are mainly used for transfers to a few African countries like Kenya and Tanzania.

It took off in those countries due to inadequate bank-card infrastructure for payments. The most famous example is M-Pesa, launched in 2007 by Vodafone. Many experts mistakenly believe that M-Pesa helped poor Kenyans with financial inclusion. In reality, the banking industry in Kenya was already rapidly expanding, and well-off consumers had one more convenient option for sending money.

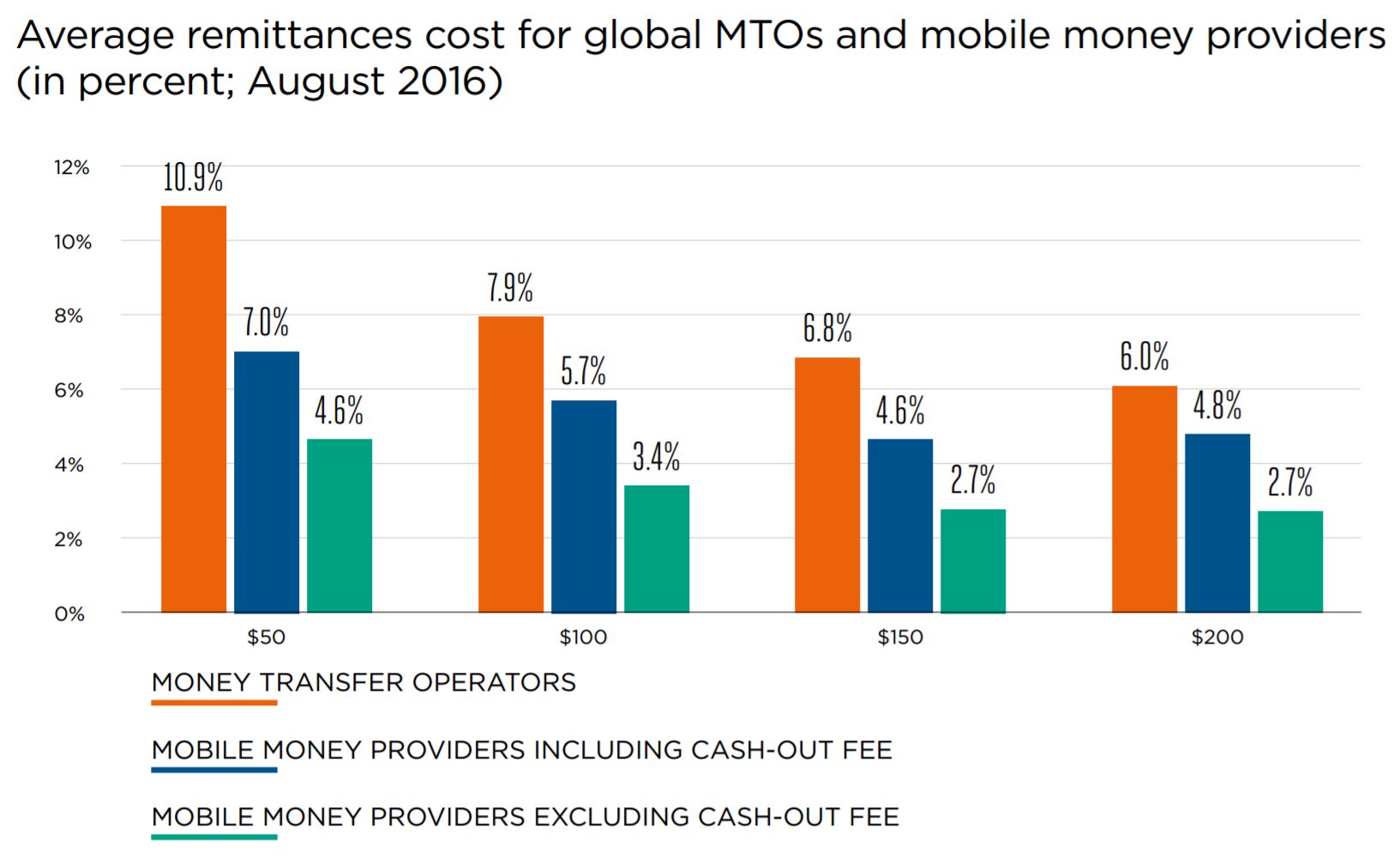

Remittance volumes among African countries tend to be relatively small and are, thus, outside the focus for digital expansion by incumbents or Fintech startups. As a result, a mobile money method could be the most cost-effective option for these corridors when compared to cash-to-cash sending:

… Back to Bitcoin/Crypto/Blockchain

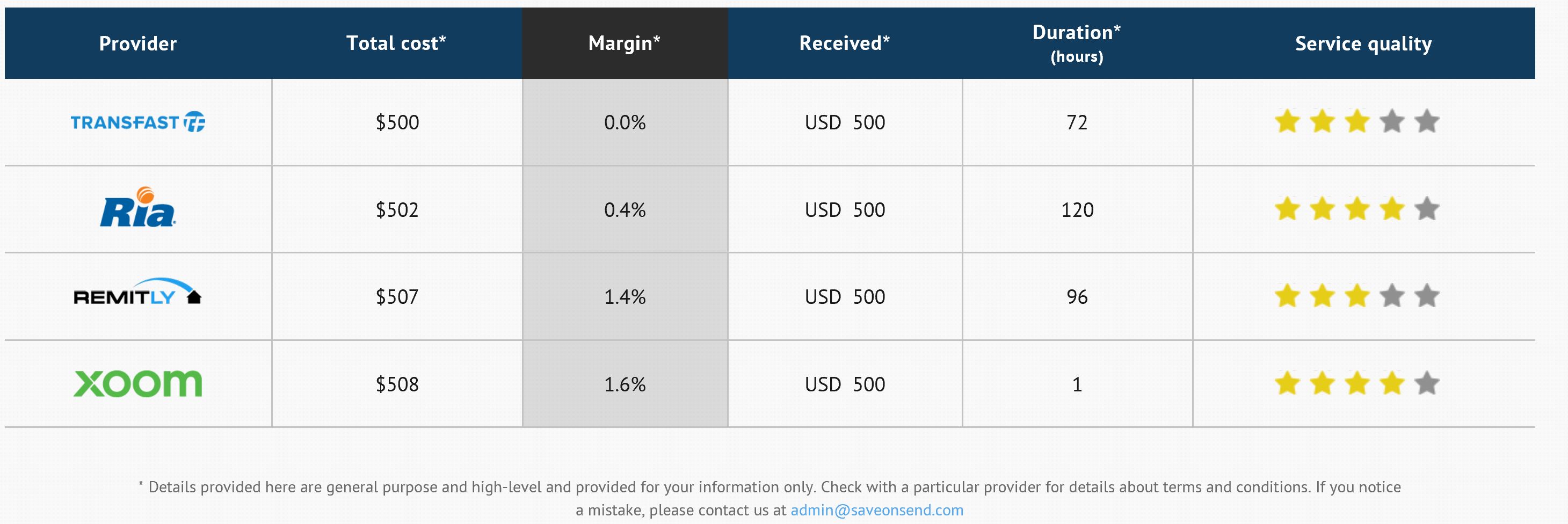

Another argument favoring Bitcoin/crypto/blockchain’s ability to reduce remittance costs is to focus on small transfer amounts. The underlying assumption is that such transfers would then dramatically increase in quantity, i.e., if it costs little to send $10 to a homeland, lots of migrants will begin initiating lots of small transfers. While some increase in smaller amount transfers has been expected (read this interview with Western Union’s executive), there is no evidence of a significant trend. Even for smaller amounts, some mainstream providers are not charging any fee, creating variable-only pricing based only on the FX markup (see top three rows in the table below). With those providers, it already costs less than $1 to send money, so even if a Bitcoin/crypto/blockchain transfer were free, the price advantage wouldn’t be enough for consumers to care:

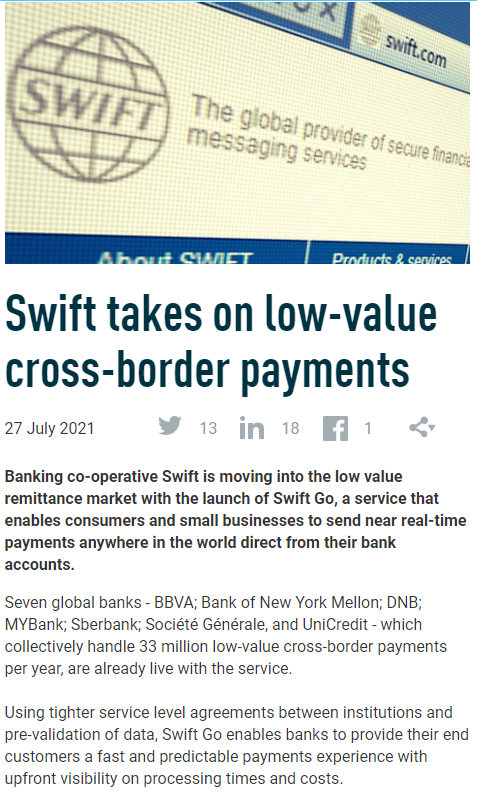

The last hope for Bitcoin’s differentiation with small transfer amounts ended in 2021 when SWIFT launched a dedicated product for that use case.

Bitcoin/crypto/blockchain can dramatically reduce correspondent banking costs

But if Bitcoin/crypto/blockchain startups can’t differentiate a direct-to-consumer service, could they be more successful as a B2B provider? Could they offer a back-end rail to the traditional money transfer operators with a significant advantage over their correspondent banking provider?

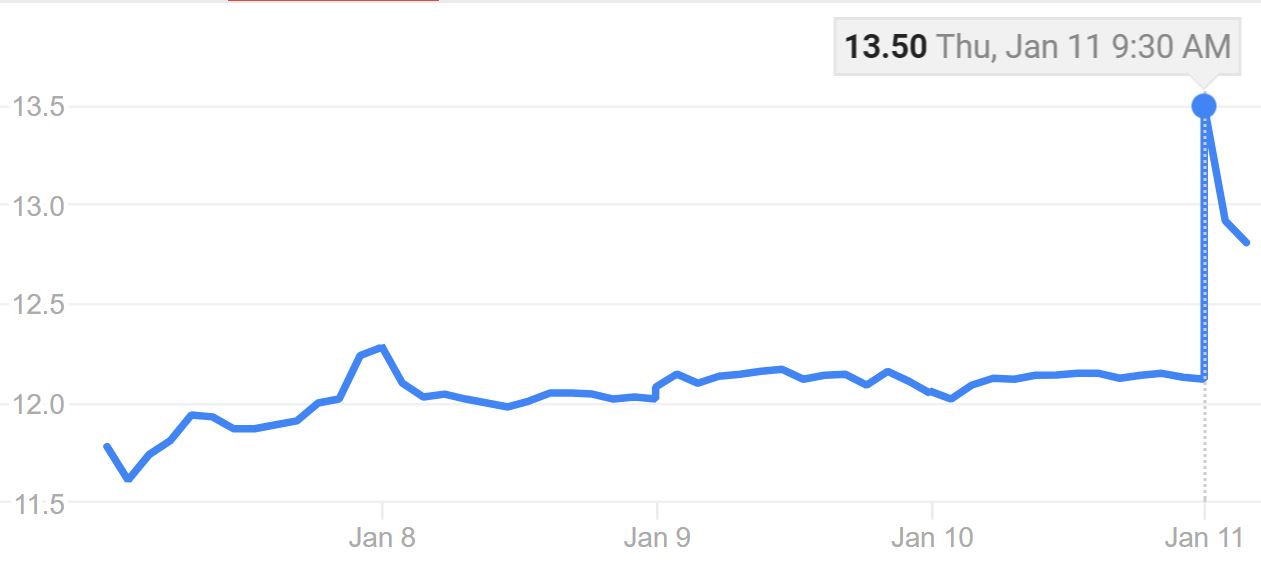

In 2015, Western Union denied rumors started by Ripple about a joint pilot. Three years later, in 2018, Western Union’s stock price jumped 10% on a similar rumor:

While Western Union didn’t pursue the partnership with Ripple, MoneyGram stepped in the same week in 2018, signing up for a pilot:

“The current model for these payments requires money transfer companies to use pre-funded accounts across the globe to source liquidity. Newer blockchain technologies have the potential to revolutionize this process and optimize capital deployment.”

source: Ripple and MoneyGram Partner to Modernize Payments, January 11, 2018

As a result, MoneyGram’s stock jumped around 10% on that day:

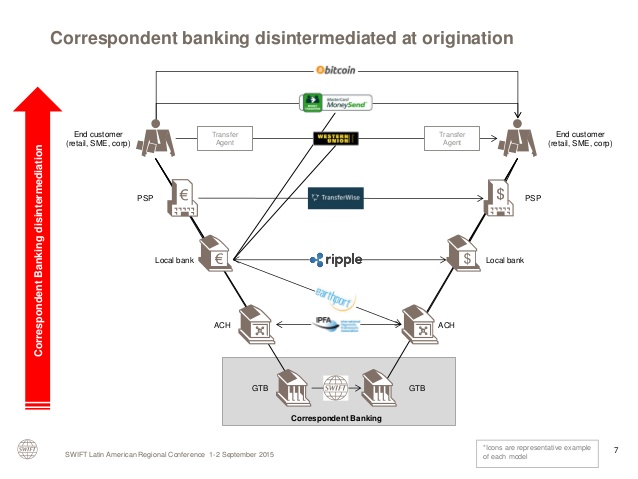

How would such a service work? A typical pitch of a Bitcoin/crypto/blockchain startup includes a picture like the one you can see below. It shows a multi-step process for customers (retail or business) who want to transfer money internationally. It then naturally proposes a blockchain-based solution that eliminates the need for all intermediaries, letting consumers and businesses interact with each other directly as they do via email:

Even while only planning a pilot with Stellar, the head of the blockchain initiative in a large Indian bank was already describing the key benefits in this article:

“This technology is enabling us to conduct business a lot quicker, cheaper with lower error rates and lower vulnerability to cyber threats. It is helping us eradicate the need for post transaction settlements which are cumbersome and expensive.”

But why, after all this time, do Stellar, Ripple, OKLink, and all other blockchain B2B providers remain so small? Even among non-blockchain B2B cross-border “disruptors,” no single player has intriguing prospects. After 20 years, Earthport’s revenue was below $50 million when it was acquired by Visa in 2019. After 15 years, CurrencyCloud’s revenue was below $100 million in 2019, when it was also acquired by Visa.

While seemingly intuitive and straightforward, two conditions would need to be met for a blockchain or fiat-based B2B solution to present a significant cost advantage over SWIFT: a) the total cost of the back-end rail needs to be a substantial component of a provider’s P&L, AND b) the existing providers are deploying those processes in a substantially inefficient manner.

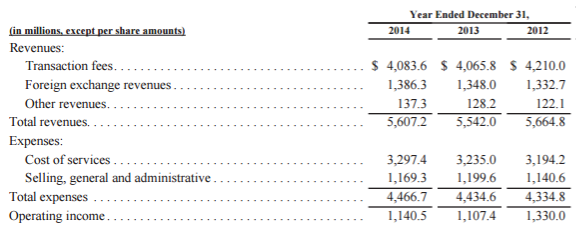

Let’s review the financial statements of publicly-traded consumer remittance companies.

It becomes apparent that most of their costs are related to payments for receiving and discharging funds to and from customers, customer acquisition, channel infrastructure, customer service, and risk-management compliance, not to recording transactions or moving money internationally (read this SaveOnSend article for more details). Hence, providers are eagerly looking for more cost-effective ways to collect and distribute funds vis-a-vis customers, acquire customers, deploy offline and online channels, service customers, and manage risks of releasing funds before getting paid, not functions where Bitcoin offers a distinctive cost advantage. For example, Western Union spent HALF of all expenses in 2014 on “agent commissions” – whether the underlying currency is fiat or Bitcoin wouldn’t make any difference.

Or, let’s consider fraud-related expenses – the central issue in the remittance industry, like the case of “employee impersonation” at Xoom, or when people lie about 1) having sufficient funds in their bank account, or 2) not sending money, or when hackers take over online accounts. Again, it is not clear why a Bitcoin-based provider would be much better at preventing such “front-end” fraud unless it is a so-called “full Bitcoin” transfer (no on- and off-ramp conversion with fiat). This will be a potentially safer infrastructure, but a very slim chance of mass adoption unless we start seeing billions of dollars spent on PR & Marketing globally.

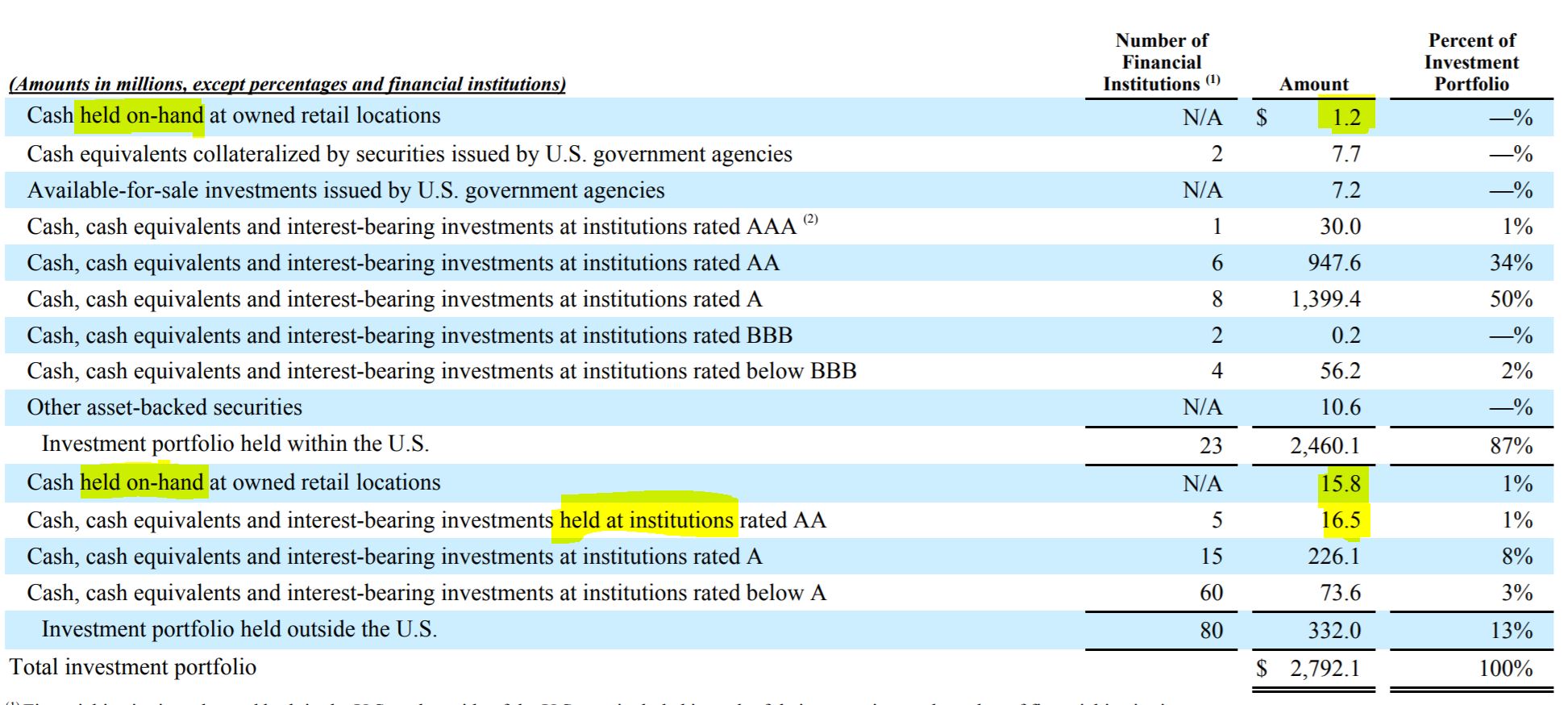

What do large remittance providers spend on correspondent banking? As we describe in this SaveOnSend article, it costs them 0.01-0.1% of revenues and is managed by a global team of 2-5 people. What would you guess was the whole pre-funding amount for MoneyGram in 2016? Around $35 million:

Compare that with their compliance activities involving 10-20% of the company staff. If a Blockchain solution replaces SWIFT in the next 10 years, it could unlock about $500 million of value annually for providers. Hopefully, they will pass half that gain to the 250 million migrants who send money home; every two dollars helps.

Nevertheless, by 2017, most large financial institutions and government financial entities were experimenting with distributed ledger technologies on Blockchain or via more private variants. Such a test-first-think-later approach had no positive surprises (examples here, here). Insufficient processing speed, low grade of security, and malfunctioning technology were normal for early tests of any new network:

“One of the main lessons from this experiment is that the versions of distributed ledger currently available may not provide an overall net benefit when compared with existing centralized systems for interbank payments. Core wholesale payment systems function quite efficiently…”

A seminal moment in the Blockchain-for-back-end debate came in March 2018 when a famed economist, Nouriel Roubini, published “The Blockchain Pipe Dream,” which included the following paragraph:

“Bitcoin is a slow, energy-inefficient dinosaur that will never be able to process transactions as quickly or inexpensively as an Excel spreadsheet. Ethereum’s plans for an insecure proof-of-stake authentication system will render it vulnerable to manipulation by influential insiders. And Ripple’s technology for cross-border interbank financial transfers will soon be left in the dust by SWIFT, a non-blockchain consortium that all of the world’s major financial institutions already use. Similarly, centralized e-payment systems with almost no transaction costs – Faster Payments, AliPay, WeChat Pay, Venmo, Paypal, Square – are already being used by billions of people around the world.”

By the second half of 2018, some incumbents began canceling their blockchain pilots. Here is the reasoning from Citi’s Head of Innovation Lab (source here):

“If we are talking about cross-border payments, how many banks do we have across the world – and how many of them are already on-boarded on SWIFT? And how long has it taken SWIFT to onboard all those banks?”

The disappointing announcements continued in 2019. Here is a typical conclusion from the experiment launched by the Bundesbank together with Deutsche Börse in 2016 and terminated in late 2018 (source here):

“The blockchain solutions did not fare better in every way: the process took a bit longer and resulted in relatively high computational costs,” Weidmann said in Frankfurt on Wednesday. “Similar experiences have been made elsewhere in the financial sector. Despite numerous tests of blockchain-based prototypes, a real breakthrough in application is missing so far.”

Bitcoin/Blockchain money transfer will destroy Western Union

Obsession with crushing Western Union seems to be a massive distraction for many crypto startups as they struggle to gain even 1% of market share in any remittance corridor. To put things into perspective, among fiat-based fintechs, only Wise, after a decade, has surpassed Western Union’s transfer volume. All others remain far behind:

The biggest rumor so far was the story from Rebit and Bloom in 2016 about a 20% market share in the Korea-to-Philippines corridor in 2016. It implied $1-2 million in monthly transfer volume among the biggest Bitcoin providers in those days, Sentbe and Payphil. Keep in mind that this particular corridor from Korea, with an overall annual transfer volume of $0.2-0.3 billion, was tiny in comparison to the top source countries for remittances into the Philippines:

Even such a relatively small volume seemed unlikely, as the central bank of the Philippines estimated the volume of remittance transactions involving ALL inbound corridors and ALL virtual currencies to be around $2 million per month at that time. The “20% market share” claims were continuously reprinted after their first appearance in September 2016, always with no evidence. In public and private interactions, SaveOnSend repeatedly asked all these startups to send us data for validation, and we are still waiting.

Eventually, the Philippines Central Bank began estimating crypto volumes for inbound remittances. By 2018, it was $8.77 million (or 0.03%), while Payphil was no longer in business.

For a while, it was common to misinform the general public about Western Union, suggesting they charged 10% for limited transfer amounts and only in the US:

In the meantime, Western Union has proven to be quite agile in its digital evolution. It was the first to provide an online channel in 2001, the first to experiment with mobile money in 2007, and the first among well-known remittance providers to invest in blockchain startups and experiment with blockchain:

As you saw in the previous comparison tables, Western Union is at times less expensive than some of the so-called Fintech startups (see this SaveOnSend article for more on that topic). For example, look at the margins across providers in one of the world’s most competitive and largest corridors, USA-to-India:

And that may be the biggest “blind spot” of Blockchain-based startups. They have an image, wishful thinking, of Western Union as a cash-only business that missed telephony and kept hanging onto the telegraph. The reality is quite different. Western Union would exploit Bitcoin-blockchain rails as soon as they become a viable alternative. Remember, profits and costs are in the first and last mile, not the rails (read this SaveOnSend article for more details). Finally, while Western Union’s market share and stock price have been slowly declining, there are yet no signs of imminent demise:

The only reason preventing mass Blockchain/Crypto money transfer adoption is [enter your favorite]

For over a decade, true believers have used the phrase “gradually, then all at once” to explain the imminence of Blockchain/Crypto adoption for money transfers. It highlights one piece of news and predicts that it foreshadows a trend:

The irony lost on these experts is that this phrasing originates from Ernest Hemingway’s The Sun Also Rises: “How did you go bankrupt?” – “Two ways. Gradually, then suddenly.” True to the classics, Tempor France was never a real remittance player. But once it pivoted to DeFi, it seemed to vanish entirely into the ether of Web3.

Rather than learning and embracing the challenging reality of consumer remittances today, these experts believe Blockchain is a “game-changer” for remittances. They are betting on a miracle of new technology taking off once enough remittance consumers hear about its features.

What would drive such mass awareness has, over the years, been some “game-changing” event; pick your favorite:

- Donald Trump becomes president and halts all remittances for undocumented migrants from Mexico.

- An economic collapse in a large country results in hyperinflation (Greece, Venezuela).

- A large retailer agrees to accept Bitcoin for money transfers.

- Bitcoin remittance startup cuts its fees and conversion rates to zero.

- Low-income consumers learn to use advanced smartphones.

- The government supports the adoption of Bitcoin (El Salvador).

- Stablecoins are regulated in the US.

Rather than asking why NO ONE is using crypto for legally sending money cross-border, including their neighbors, families, and friends, the payment industry pundits prefer to wonder about poor people in mysterious Africa (read more here):

“Potentially, Africa’s huge unbanked population combined with the burdensome process of opening and operating a bank account should make Bitcoin an instant hit. However, its adoption has been irritatingly slow even though the basic infrastructure is not missing. It is estimated that by the end of this decade that 80 percent of the continent’s more than 1.2 bln population would be using Smartphones. Then what hinders Bitcoin penetration in Africa?…”

Crypto’s adoption in other use cases

The lack of any noticeable Bitcoin adoption is a sobering reality 16 years after the release of Version 0.1. It is evident across all regions and use cases, not just remittances. Are you old enough to remember the exuberance in 2014 when thousands of merchants agreed to accept Bitcoin? But 3 years later, in 2017, the verdict was in:

- CheapAir.com: “…it certainly hasn’t taken off…”

- Dish Network: “…we have not seen growing enthusiasm…”

There were still some merchant processors reporting fantastic growth. Here are the headlines from BitPay’s report on achievements in 2017:

- on pace to process over $1B annually in bitcoin payment acceptance and payouts, and we’ve already grown our payments dollar volume 328% year-over-year from 2016

- NewEgg has more than doubled its Bitcoin sales from last year

- seen a more than doubling in transactions going to Latin American merchants since August of last year

- the US card program alone grew by 1583% year over year (from August 2016)

Looks impressive, right? However, BitPay conveniently did not mention either a base for comparison or the number of active customers and transactions. A dollar volume growth of 300+% % would be impressive for a regular merchant processor. For a Bitcoin-based provider, when Bitcoin’s value has grown 1,000-2,000% in the previous year, such a “growth” number seems more like a loss. By 2018, any optimism was gone despite lower fees (source here):

While the crypto impact has been invisible for legal money transfers, e-commerce, or in-store purchases, several use cases represent a lion’s share of all usage.

- Legal but with no intrinsic value: 1) investing in cryptocurrency, 2) trading on price discrepancies across exchanges.

- Illegal but with intrinsic value: 3) ransomware, 4) money laundering, 5) tax evasion, 6) Ponzi schemes.

By definition, no one can know the volume of illegal cross-border transfers/payments. One of the most prominent industry experts, Hugo Cuaves-Mohr, estimated it in the $150-200 billion range. For a 10-15% premium, tax evaders buy Bitcoin for cash in countries like India and China, then sell it on exchanges in a developed country (Bitstamp or Kraken) and deposit laundered money there. Because of Blockchain/Bitcoin’s widespread role in money laundering and tax evasion, the US tax authority (IRS) requested the names of Coinbase customers in late 2016 and won the case in court in late 2017.

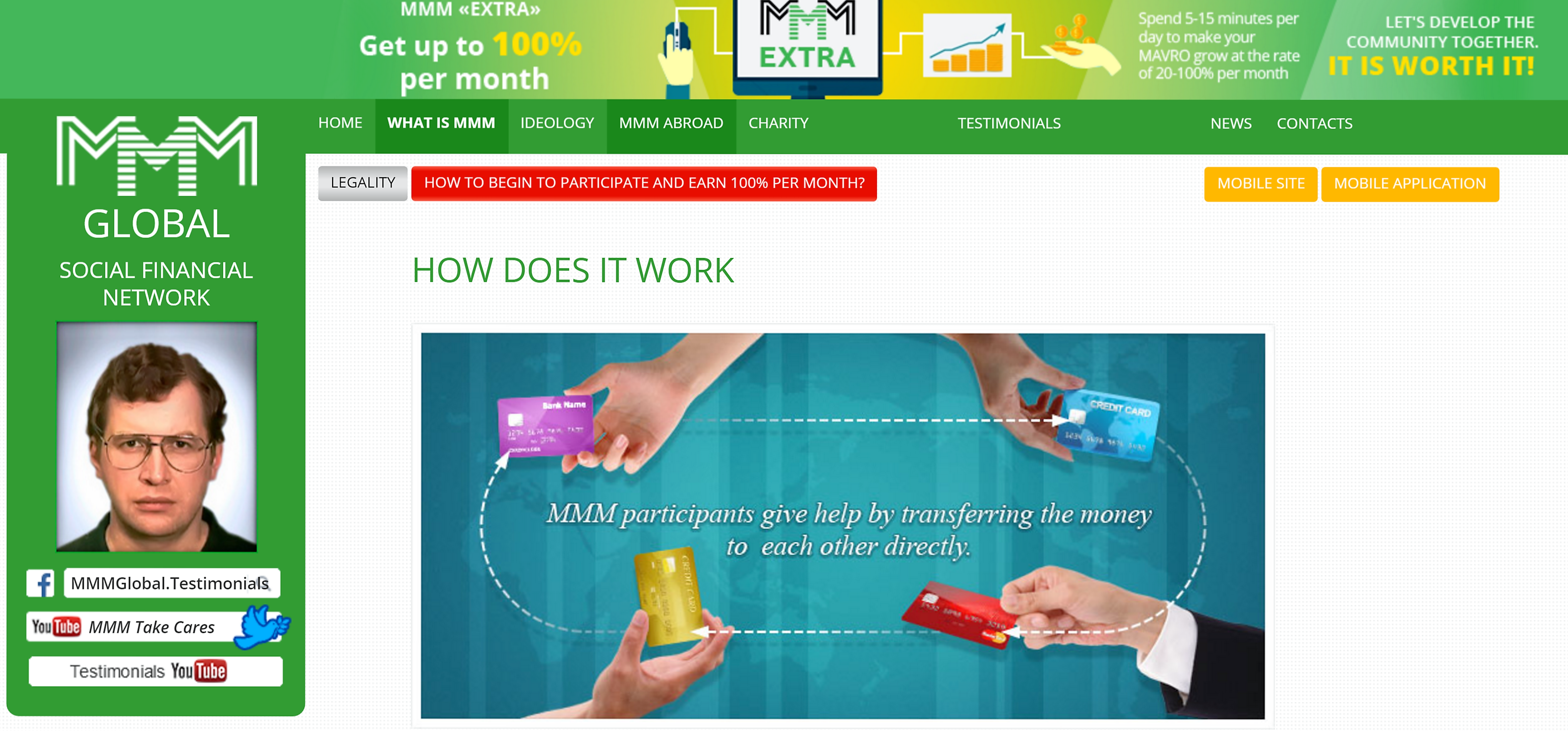

Until the death of its founder in 2018, a clear leader among Ponzi schemes was MMM, claiming 250 million users in 118 countries, 3 million in Nigeria alone. MMM accomplished it while hiding from governments, with cheap websites and an offline agent network. Watch this short video and ask yourself why not a single crypto startup for cross-border money transfers has been able to accomplish 0.1% of the MMM scale:

Even more grounded Blockchain/Bitcoin supporters felt it was reasonable to compare Bitcoin with Skype, WhatsApp, and other world’s biggest consumer platforms:

The irony of the above meme (created in early 2016 and resurrected in late 2017) is that no one who seriously shared it was using Bitcoin as their primary bank. Why? They seem to forget the two most basic principles behind the success of any innovation:

- A manifestation of product-service virality takes weeks/months, not years. WhatsApp and other “viral” giants spread like fire to millions of users and didn’t require second-guessing. Nothing even remotely close has been transpiring with ANY crypto apps, and the active user base of the ones focused on remittances is typically measured in hundreds.

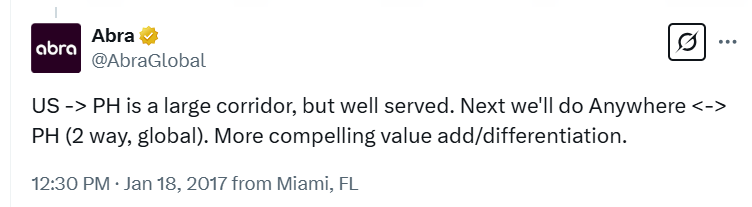

- The happier consumers are with their existing choices and the more work they require to adopt, the more branding and marketing efforts crypto providers have to make to initiate said adoption. They should also embrace the harsh implication that an abundance of satisfactory options impedes adoption among customers and necessary business partners. Why would a grocery store engage with a new provider with a minuscule remittance flow if they already have a satisfactory working relationship with Western Union and other well-known brands? Read how CEOs and founders of Bitcoin remittance startups described this particular challenge: BitSpark, Abra, and Rebit.

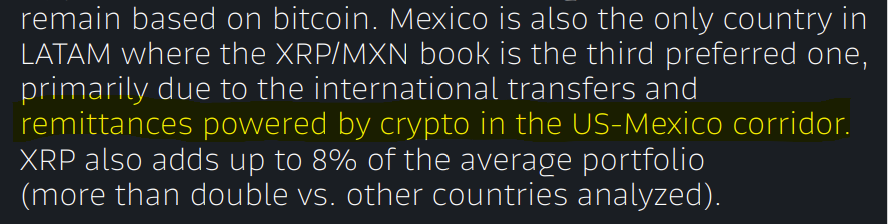

Any claim of crypto adoption for remittances should be taken with a grain of salt. One of the most prominent examples of supposed success is Bitso. This Mexico-based crypto exchange claims billions in remittance transfers, mainly from the US to Mexico. However, international money transfers are licensed and heavily scrutinized by government agencies. If millions of consumers send monthly remittances in crypto, why is no licensed operator (MTO) taking credit for adopting such groundbreaking innovation?

In early 2024, Bitso published a report stating that Ripple was a major contributor to that remittance volume. Given Ripple’s history with MoneyGram, this raised even more questions about whether these transfers are legitimate or part of a pay-per-play scheme to inflate XRP liquidity artificially in Mexico.

By mid-2024, Bitso claimed that over 10% of U.S.-to-Mexico remittances were moving via crypto rails. Yet again, requests for substantiation or transparency regarding these bold claims went unanswered.

El Salvador’s failure with Bitcoin for remittances

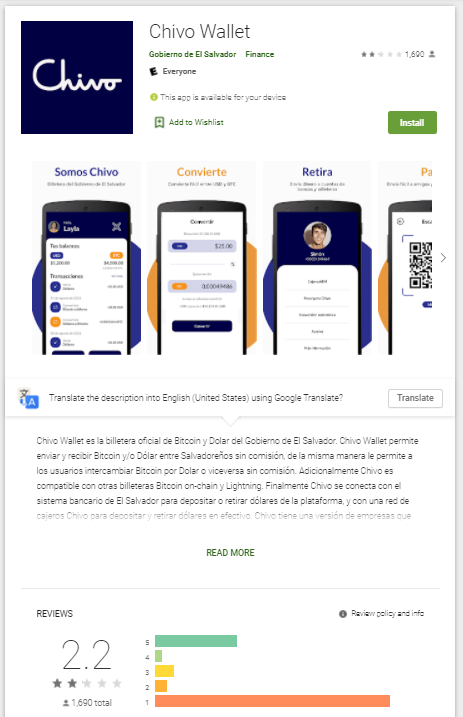

So the most significant barrier to mass adoption might be that the crypto community still lacks skeptical practitioners who would consider a new payment rail and cryptocurrency to be just another novelty and know how to win against the headwinds. But time and time again, the execution is lacking. When El Salvador embraced Bitcoin as legal tender and encouraged remittance users to switch from their existing providers in 2021, here was the quality of the official Bitcoin wallet:

Even more shocking was the reaction from crypto heavyweights. For a decade, they have been dreaming about governments not impeding the adoption of Bitcoin and other cryptocurrencies. El Salvador moved beyond anyone’s wildest dreams by paying citizens to download a Bitcoin wallet and pressuring merchants to accept it. Has any major player opened an office in El Salvador, moved there, pitched in with marketing to persuade Salvadorans in the US to send remittances via this new rail, or assigned their best developers to improve the Chivo wallet? Nope.

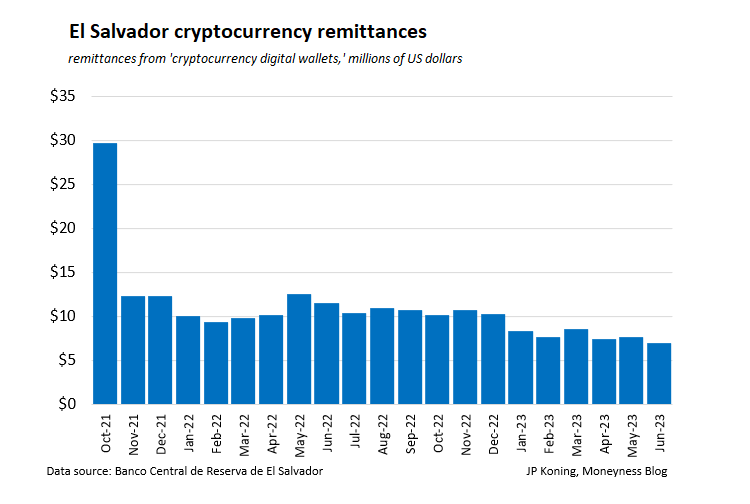

The results were predictably disappointing, with Bitcoin remittances in decline since their launch in 2021, falling to around 1% of monthly volume:

Instead of a hands-on attitude in seizing this opportunity of a lifetime, we keep hearing from idealists stuck in the “Bitcoin=Internet” paradigm. Whether it is a new brand of vodka, clothes, car, or remittances, the real “game-changer” is in superb execution of a more-or-less standard playbook. Miracles are known for tardiness.

Specific examples of Bitcoin money transfer providers

Graveyard – closed or pivoted away from cross-border consumer money transfers:

- October 2020: Rebit.ph shuts down after raising $100K in 2015. It generated around 100 daily transactions making money on the FX-Bitcoin spread. Read this article from its former insider.

- October 2017: Bitspark pivots to B2B (investors: RGAx), shuts down completely in March 2020

- July 2016: Freemit shuts down (investors: Alchemist Accelerator)

- January 2016: Romit shuts down (investors: 500 Startups, AltaIR Capital)

- November 2015: BitPesa pivots to B2B (investors before pivot: DCG, Pantera).

- Launched in 2013, BitPesa initially was the best-known “use case” for Bitcoin consumer remittances to a few countries in the middle of Africa. However, as BitPesa struggled to gain traction among consumer remittance users, it discovered that its typical early adopter was a small business owner who occasionally sent money.

- Facing this reality and struggling in the initial outbound market, the UK, BitPesa expanded its marketing efforts to potential senders from other countries like Canada and the USA and began targeting B2B cross-border payments (see an informative presentation by BitPesa’s CEO).

- BitPesa raised close to $2M initially, and its transfer volume grew at 30%/month from $50K in January 2015 to $400K by July. As of November 2015, nearly all its customers used BitPesa for business needs.

- October 2015: Bitstake->NairaEx

- August 2015: Beam shuts down (investors: MTT Group)

- July 2015: Cryptosigma->Toast (investors before pivot: Startupbootcamp)

- June 2015: 37Coins shuts down (investors: 500 Startups)

- April 2015: Buttercoin shuts down (investors: Google Ventures, Y Combinator)

- 2015: HelloBit shuts down (investors: 500 Startups)

Abra (A Better Remittance App) deserves special mention in this section.

When, on September 10th, 2015, Abra announced that it had raised $12 million in funding, it marked a seminal moment for Bitcoin’s evolution in remittances. For the first time, there was a startup with enough funds to acquire 100,000+ remittance customers. This made Bitcoin for remittances no longer a hypothetical question. We were finally able to compare Abra’s progress with the initial trajectories of established remittance startups:

- TransferWise: raised $7 million in its first 2.5 years, reaching $35M in monthly transfer volumes

- WorldRemit: raised $7 million in its first 4 years, reaching $50M in monthly transfer volumes

- Remitly: raised $11 million in its first 3 years, reaching $2M in monthly transfer volumes

By August 2017, two years later, Abra had only 73 users a day…

Abra’s vision was groundbreaking: enabling consumers to act as ATMs to eventually replace hawala and catalyze a faster shift from offline to online methods of sending money. Abra was not looking to modify end-users’ behavior; it aimed to enable a cash-to-cash method habitual for 90% of remittance transactions at the time. The fact that Bitcoin was somehow involved was also purposely hidden from consumers.

Abra was launched in February 2015 with a fascinating premise but a comical-borderline-bizarre pitch. At that point, it was hard to imagine a better parody of the disconnect between Bitcoin’s ardent fans and the reality of money transfers than this presentation and the follow-up reaction. Please watch it; it’s only 6 minutes:

This pitch won the 2015 “LAUNCH Festival” Award. Moreover, the Abra app was hailed as the finally arrived “Uber for remittances” and “Western Union killer.” If you were not inside the Bitcoin bubble, you could be forgiven for chuckling a few times while watching the video. Abra’s presentation started with: “I wanna talk to you about a Mexican immigrant named Bill” and painted a story of the human suffering of someone in Mexico who must “drive 2.5 hours” to the nearest cash agent. Abra had a solution for those greatly inconvenienced folks: “human teller.”

Considering the ubiquity of cash agents, it is not hard to imagine a place that is so remote. There are numerous small villages, with 50-100 residents, in such hard-to-reach places that remain there for historical rather than economic reasons. For anyone who ventures to such villages, a few gaps become apparent in Abra’s presentation: a) Mobile data connectivity, which could be spotty even around large cities, is usually non-existent once you are this far from larger cities and infrastructure; there is just no business case for deploying such capabilities. b) Comfort and trust in technology, especially regarding money, are far behind in their evolution. c) While living in those communities is usually very safe, the overall protection coverage by the government is quite limited.

There might be an eager early adopter segment: criminals. Finally, an app for them could quickly identify somebody with money in the vicinity and thus significantly improve the effectiveness of victim targeting.

However, investors who gave Abra $12 million were not inclined to waste money by targeting remote villages. Helping the “poor” is good PR, but like all other Fintech startups, Abra was also going after tech-savvy consumers in major metropolitan areas of top global remittance corridors. It quickly became apparent that “P2P” was also just PR. Most of Abra’s distribution in the Philippines was not through “human tellers” but the same pawn shops used by traditional remittance providers.

From the beginning, there was also an obvious question about Abra’s ability to make a profit, considering that they charged 0.5% on each transfer side, assuming all FX risk. At that point, Bitcoin spreads were high, and hedging was very hard to find; hence, it was pretty expensive (Bitcoin mining businesses in developing countries were already looking for the same hedge). If we add Abra’s gross margin and each side’s markup of 1%, the total margin gets to around 3%, which was on the high end for corridors like USA-to-Philippines:

Abra started by trying to sign up thousands of “human tellers.” The startup’s initial focus was on the USA-Philippines corridor, which was in the bull’s eye of all traditional players and fintechs. Just nine months after getting funded, Abra pivoted to a different offering: a typical Bitcoin wallet focusing on consumers with linked bank accounts and offering cash-out via convenience stores. Here is how Abra’s founder explained that pivot a couple of years later, in 2018:

“People were starting to use the tellers to actually buy bitcoin,” Barhydt said. “Our customers [were] pulling us to basically become an investment vehicle…

Sixteen months after a $12 million funding round, Abra all but gave up on its original pitch. It focused almost exclusively on a wallet play and pitched it as global domination:

Ultimately, Abra’s initial focus on remittances became a repeat of another venture in the same space, Boom Financial. Founded in 2008 by Abra’s management, Boom was pitched as “the first cross-border mobile banking service in the US” (on a side note, same as claimed in 2012 by Remitly). From 2008 to 2012, Boom raised $28 million from RRE Ventures and others, and… nothing.

Out of all the failed Bitcoin remittance startups, Abra’s pivot was the most disappointing. On paper, its target segment and user experience were distinctive and had the promise of making a real change for a large portion of cash remittance users. Instead, Abra became another mundane wallet app for better-off consumers with bank accounts. In just 2 years, Abra’s focus changed from helping “Mexican named Bill” with cheap remittances to helping affluent American Express cardholders invest in Bitcoin for a 4% fee:

In October 2017, Abra raised $16 million to offer credit installments. Here is how Abra’s founder explained their failure in cross-border transfers:

Still Active B2C Startups:

bridge21

The startup, bridge21, was launched in January 2017, targeting the world’s largest remittances corridor: USA-to-Mexico. It tried capitalizing on the difference in Bitcoin pricing between the USA and Mexico, at times offering a below interbank exchange rate, surpassing all competitors:

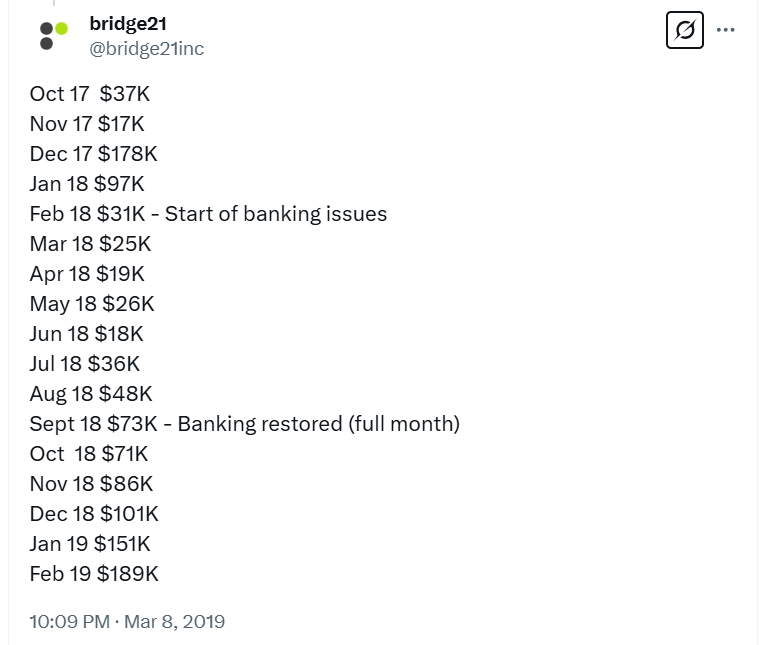

bridge21 faced challenges in its early years due to issues with the banking provider and the global decline in Bitcoin liquidity. As a result, transfer volumes did not increase significantly. However, it’s worth noting that bridge21 was the only Bitcoin/Blockchain startup globally that initially shared its revenue, although it stopped doing so after early 2019:

Other interesting startups to follow:

Regulatory aspects of using Bitcoin for money transfer

Compliance with KYC-AML regulations poses an existential question for crypto remittances. Even for fiat-based transfers, banks routinely cut off small remittance providers and express serious concerns about doing business with even the largest players. A senior banker described reasons why their bank wouldn’t open a correspondent account for a crypto-based provider of remittances:

“Our bank is careful NOT to aggressively address new frontiers given potentially high penalties or even simply being in a penalty box by regulators. Concerns are obviously similar to those with regular providers of remittances: money laundering, gambling, drugs, or within other prohibited industries. Unfortunately, I don’t see a path forward in the near term: we won’t be able to monitor or control their flows even if we were to hire more people in compliance or invested more in the systems.”

Read this article on whether such compliance is even feasible. Faisal Khan discusses various aspects of Bitcoin’s legality and compliance for sending money internationally in his “The Lure of Remittances for Bitcoin Startups” article. Some providers hope that if they are MSB-licensed outside the US, they could have an online website and provide money transfers from the US to their country. Finally, read his step-by-step instructions on how to make Bitcoin an international money transfer compliant.

For Bitcoin regulations in the US, state-by-state, read here.

Overall, it is understandable why a cross-border remittance provider requires more scrutiny than a company in a lending space like Lending Club or Affirm. The additional risk of money laundering and terrorism financing might outweigh any potential benefits. At the same time, there is a risk of applying excessive regulation to this seemingly promising innovation (FinCEN Fines Ripple, Wells Fargo shuts down Bitfinex transfers, “Bitcoin Still Confuses Bankers“).

Simultaneously, the crypto ecosystem must significantly intensify its efforts to combat criminals exploiting this innovative technology. Instead of frequently hearing excuses about anonymity, there should be a proactive termination of criminal activities. Cases of identifying tax evaders among customers by Coinbase, Kraken, and Bitstamp are notably absent.

In the instance of a global Ponzi scheme by MMM, it was technologically feasible to identify and shut down the accounts of the scheme participants. This massive scam disproportionately targeted low-income consumers in Africa and Southeast Asia. The governments of affected countries took urgent action in response to the Ponzi scheme. Despite the frequent discussion within the crypto community about caring for the less fortunate, there is a question about what specific measures were taken to prevent or address this fraud:

In Conclusion: Making crypto money transfers a reality

After 15 years of missed opportunities, the crypto community must acknowledge that frictions in consumer cross-border money transfers have diminished due to a combination of government, bank associations, and fintech efforts. The remaining pain points are limited in scale, and implementing a crypto solution would encounter significant regulatory uncertainty. This doesn’t imply giving up on the market but necessitates making large, concentrated bets with hands-on involvement.

In 2019, Ripple demonstrated that with a quarterly investment of $10 million, they could acquire 20% of the liquidity of the top-3 remittance firms in the world’s largest corridor. Similar arrangements were made with smaller players in the US and Europe. Ripple utilized these artificial measures to encourage consumers to buy XRP and persuade regulators to approve their IPO plans. Some major Bitcoin miners could afford similar liquidity purchases, with top miners potentially joining forces, investing 5-10 times Ripple’s capital, and acquiring equity ownership in major fiat money transfer operators while compensating them for liquidity.

While this approach may sound like socialism and require additional paid lobbyists for SEC approval, top Bitcoin miners already have a viable business model and may not be planning an IPO. However, there’s a recognition that adoption won’t happen otherwise. The long-term vision for crypto-based remittances involves stabilizing currency in the next decade, paving the way for a new wave of startups promoting Bitcoin as a store of value and investment. Although these startups may burn out, they might set the stage for the mass adoption of Bitcoin, potentially including a “killer” remittance app.

If you know of a crypto-based remittance provider with substantial volumes, please share details in the comments.